National Commercial Bank (NCB)shares may not be trading in droves recently with the price tending to trade around $17 since early May but investors may be missing a great buying opportunity with a stock that is seriously undervalued.

National Commercial Bank (NCB)shares may not be trading in droves recently with the price tending to trade around $17 since early May but investors may be missing a great buying opportunity with a stock that is seriously undervalued.

In Trinidad the stock closed as low as TT$1.04 recently but has moved up to $1.10 on Friday and seems poised to go higher. The bid in Trinidad on Friday close was $1.10 (J$19.20) to buy 22,933 units with an offer of 26,000 units at $1.14. On Wednesday the stock traded 69,456 units at $1.08 and gained 2 cents in the process. On Friday 21,322 traded in Jamaica at $18.01 each and 1,396,013 on Thursday between $17 and $18.03. Wednesday saw 21,595 units being traded between $17.30 and $19. One important factor is that the stock is not in great supply.

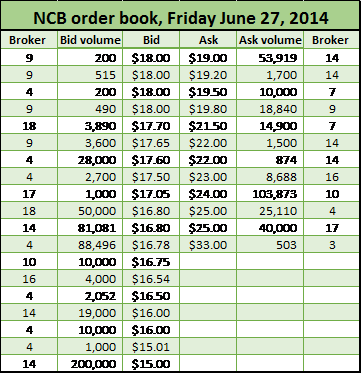

But it’s the order book on the Jamaica Stock exchange that is sending a strong message to buy coupled with is a year when the results should help stimulate the stock price higher. There are only 280,000 shares on offer in the market but the buying interest is not particularly strong. With the pickup in trading in Trinidad, the price in Jamaica could get a lift and with third quarter results to June which are due in the last week in July, that could strengthen investor’s appetite for the stock and give it a badly need push.

But it’s the order book on the Jamaica Stock exchange that is sending a strong message to buy coupled with is a year when the results should help stimulate the stock price higher. There are only 280,000 shares on offer in the market but the buying interest is not particularly strong. With the pickup in trading in Trinidad, the price in Jamaica could get a lift and with third quarter results to June which are due in the last week in July, that could strengthen investor’s appetite for the stock and give it a badly need push.

IC Insider forecast earnings of $5 per share for the current year, so far NCB reported earnings of $2.38. For the first 6 months of the fiscal year.

H&L profit up 310%

Profit after tax at Hardware & Lumber (H&L) was $40 million for the three months ending March this year, a 310 percent increase over the $10 million for the same period in 2013 resulting in earnings per share of 50 cents, compared to 12 cents for the comparative period in 2013. Return on equity based on the first quarter results is 13.6 percent, based on IC Insider’s projection of $434 million or $5.40 per share for profit after tax for 2014, the return on equity should hit a strong 31 percent.

Profit after tax at Hardware & Lumber (H&L) was $40 million for the three months ending March this year, a 310 percent increase over the $10 million for the same period in 2013 resulting in earnings per share of 50 cents, compared to 12 cents for the comparative period in 2013. Return on equity based on the first quarter results is 13.6 percent, based on IC Insider’s projection of $434 million or $5.40 per share for profit after tax for 2014, the return on equity should hit a strong 31 percent.

Revenue| Sales for the 2014 quarter was $1.81 billion, 17 percent more than the $1.55 billion achieved in 2013. According to management in their report to Jamaica Stock Exchange” revenue in the ‘Household, Hardware and Building Products’ segment increased by 16.7 percent while the ‘Agricultural Products and Equipment’ segment recorded growth of 17.7 percent. All of our merchandise categories did well, led by the building supplies division which delivered significant revenue growth, albeit at lower margins. The overall improved performance was realized in both the wholesale and retail divisions of the business through the expansion of product assortment, improvements in availability and by working closer with our customers to better understand and supply their needs”.

Gross profit| H&L achieved $411.5 million in gross profit or a meagre one percent gain over the corresponding period in the prior year. “The average margins declined by 3.6 percent, due primarily to the sales mix and higher product costs. Total operating expenses were $376 million or 4.6 percent lower than the comparative period in the prior year. The company realized savings in pension and other retirement benefits costs from the changes to the benefits programmes implemented at the end of 2013. In addition, several categories of expenses including staff costs, utilities and repairs and maintenance expenses were reduced through ongoing process improvement and cost containment”

“Net current assets increased by 12.4 percent to $1.05 billion, caused mainly by increased inventory and accounts receivable balances. The value of inventory increased to $1,448.4 million, partly due to the higher cost of the United States dollar as well as a desire to maintain adequate inventory levels to ensure consistent product availability for our customers” management indicated.

At the end of March, cash was $313 million representing a decline of $45 million when compared to the balance at March, 2013, equity stood at $1.2 billion.

Dolphin boost Profit 26% – Buy Rated

In a period when many junior market companies reported lower profits, the entertainment company Dolphin Cove enjoyed a robust 26 percent increase in profit in the first quarter of 2014 with profits after tax rising to $148 million an increase of $33 million compared to the 2013 March quarter from an 11 percent increase in revenues to $436 million over the 2013 first quarter amount of $394 million. While overall revenues climbed 11 percent it was the attractions that delivered increases with an 18 percent gain as the other main income source was flat with earnings of $149 million in both the 2013 and 2014 periods. Management indicated that their investment in sales and marketing helped to produce the favourable results. The revenue gains took place in the period that did not include the Easter holiday which fell in April this year compared with March last year.

In a period when many junior market companies reported lower profits, the entertainment company Dolphin Cove enjoyed a robust 26 percent increase in profit in the first quarter of 2014 with profits after tax rising to $148 million an increase of $33 million compared to the 2013 March quarter from an 11 percent increase in revenues to $436 million over the 2013 first quarter amount of $394 million. While overall revenues climbed 11 percent it was the attractions that delivered increases with an 18 percent gain as the other main income source was flat with earnings of $149 million in both the 2013 and 2014 periods. Management indicated that their investment in sales and marketing helped to produce the favourable results. The revenue gains took place in the period that did not include the Easter holiday which fell in April this year compared with March last year.

Operating expenses for the quarter was held to 8 above the prior year although there was increased Expenses in sales and marketing and devaluation of the Jamaican dollar. There was a reduction in the direct cost of dolphin attractions due to savings in the rental costs as a result of the purchase of seven previously rented dolphins, offset by additional depreciation and interest cost.

The company would have benefited from the fall in the value of the local currency as its income is denominated in United States dollars but much of its cost is ion Jamaican dollars. But the end in not yet in sight for the fall of the local currency as the country will enter the low inflows and high demand period starting in September, Dolphin stands to further benefit from this movement with income increasing and local cost kept under control.

The company’s income is substantially reliant on developments in the tourism sector as it get the bulk of its income from overseas visitors.

IC Insider’s forecast for earnings is $1.20 per share for the current year which end in December, last year the company earned 82 cents and paid out almost 50 percent of profit as dividends.

Equity stood at $1.44 billion at the end of March with borrowed funds at only $316 million.

The company owns properties in the Turks & Caicos Island and St Lucia where it intends to operate its attractions when implemented and fully operational these should add to revenues and profit down the road.

Guardian Media profit drops

Trinidad’s Guardian Media (GML) reported profit after tax that declined to $3.8 million for the first quarter this year from $7.3M in the March 2013 quarter. The media group generated revenues of $44.5 Million for the first quarter compared with $46.1 million earned for the corresponding period in 2013. , The 2013 revenue benefited from advertising relating to election campaigning in that year. The March quarter is not the best in the media business coming after the high advertising Christmas period .

Management indicated in their report to shareholders that the 2014 results was impacted by lower revenues and increased operational costs including the acquisition of the West Indies home series cricket rights for the next six years.

Our Balance Sheet continues to strengthen with increases in net assets of $42.2 Million moving from $273 Million in 2013 to $315 Million in 2014 and cash reserves increased by $3.8 Million over the comparative period.

According to management investments made to date in talent, products and capacity enhancement, and a positive outlook for the economy in 2014, they are confident of achieving the budgeted projections for 2014. They did not disclose what their forecast is but IC Insider expects the company will earn close to the results for 2013 of TT$45 million.

Trinidad PE moving slowly

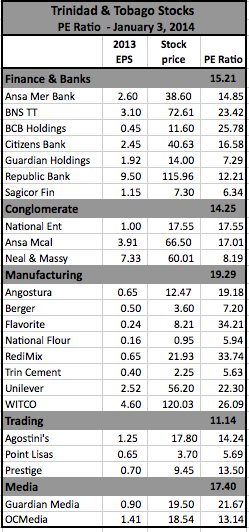

Friday, 3rd January 2013 | The only significant movement to take place during the week on the Trinidad Stock Exchange is the continued rise in the stock price of First Citizens but that had little effect on the potential gains for the company as shown on our PR Chart. The stock closed the week at a record $72.61 price.

For others that had gains during the past week, the movements were even less impactful on potential gains. Trinidad Cement’s gain during the week helped to reduce the gains going forward while Republic Bank keeps inching up but still has much room to cover before it becomes fully valued.

For others that had gains during the past week, the movements were even less impactful on potential gains. Trinidad Cement’s gain during the week helped to reduce the gains going forward while Republic Bank keeps inching up but still has much room to cover before it becomes fully valued.

By the looks of the IC Insider PC Chart to start off the New Year, the Trinidad market is poised to enjoy another year of healthy gains for some stocks.

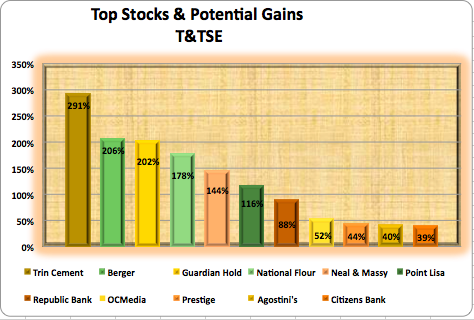

The Top Stocks with potential gains by PE Ratios are Trinidad Cement leading with 291%, Berger 206%, Guardian Holdings 202%, National Flour 178%, Neal & Massy 133%, Point Lisa 116%.

The Top Stocks with potential gains by PE Ratios are Trinidad Cement leading with 291%, Berger 206%, Guardian Holdings 202%, National Flour 178%, Neal & Massy 133%, Point Lisa 116%.

Stocks with less than 100% potential gains are Republic Bank, OC Media, Prestige, Agostini and Citizens Bank, who has given investors over 96% gains (including dividends) in the 5 months since listing as an IPO in August, 2013.

Related Posts | First Citizens staff lose huge payday | Buy Rated: H&L up 74%

Access moved to Market Watch

Friday, 20th December 2013 | IC Insider has moved Access Financial to the Market Watch list with a hold placed on the stock for the time being as the recent price movement has moved the stock close to full valuation based on estimated 2013 earnings. The Junior Market stock should be held as supply is very low and the price should move up further.

IC Insider projects $1.70 per share earnings for 2014, which means that there is still room for growth, but the potential for price appreciation lags the majority of stocks in the market currently and, therefore, it no longer deserves a Buy Rating accolade. Access Financial has gained 36 percent since being tagged as Buy Rated on the 15th of July. Access also paid a dividend of 31 cents per share on August 15, bringing the total gross gains to 40 percent.

Elsewhere, the list remains as it was although the prices of some of the selections have moved up in the last week. There are strong signs that the prices of many of the selections, particularly those in Jamaica, will move up prior to the year end. This week, the Jamaica stock market closed with 12 stocks having bids above their last selling prices.

Lasco Manufacturing remains on the list not because of 2014 earnings which are unlikely to be very price positive, but based on the implications for revenues and profit with the start-up of operations of the new and expanded factory. This should be positive for the 2015 fiscal year ending in March.

Related posts | Access growth continues | LASCO manufactures more profits

Related posts | Access growth continues | LASCO manufactures more profits

Buy Rated: More stocks performing

Friday, 20th December, 2013 | As the year grinds to a close, more of the Buy Rated stocks are showing growth. One such is Access Financial Services, which IC Insider placed a hold on and moved to the Market Watch list.

Caribbean Producers’ price has moved up to $2.60, a 28 percent gain since September when it was placed on the Buy Rated list. Meanwhile during the past week, the Lasco companies have reduced the level of losses suffered in November. Carib Cement has moved up with a 10 percent gain since selection in November and is expected to record further gains with the announcement of a price increase and exports to Venezuela.

Jamaica Broilers moved up in the week to $4.51 thus reducing some of its losses, while Grace continues to bob and weave between $56 and $63. Others in the main market have been trimming their losses of recent months and are expected to continue to do so for the rest of the year.

Jamaica Broilers moved up in the week to $4.51 thus reducing some of its losses, while Grace continues to bob and weave between $56 and $63. Others in the main market have been trimming their losses of recent months and are expected to continue to do so for the rest of the year.

On the Trinidad market, Scotia Investments fell 13 percent during the week from the Buy Rated entry point. Most others remained relatively stable. There are now 3 losses in the Trinidad section while there are 8 winners.

Related posts | Access moved to Market Watch

Buy Rated misses & gains so far

Friday, 11th October 2013 | This past week was not a great one on the Jamaica Stock Market as the market dropped starting from the previous week’s Thursday until this past Thursday, only partially offset by a rally on Friday. The Trinidad Market held its own with a few days when advancing stocks out numbered declining ones by some margin.

JMMB and Grace Kennedy climbed 14 percent and 25 percent, respectfully, on the Trinidad & Tobago market while Sagicor Finance is up 7 percent and Scotia Investments up 4 percent since we placed them on the Buy Rated list.

Guardian Holdings is down by 8 percent and Neal & Massy by 4 percent and stand as the only two losers of the selected Buy Rated list for the Trinidad Market.

Things have not gone as well in the Jamaican market with 4 stocks showing double digit losses but the majority have held close to the selection price.

Things have not gone as well in the Jamaican market with 4 stocks showing double digit losses but the majority have held close to the selection price.

The Buy Rated list has a new stock for investors to consider on the T&TSE. Point Lisas Port Development has been added to based on profits so far this year, which suggest earnings of approximately 40 cents per share from operations and a current price of $3.77, could double in price.

Related posts | TTSE PE: Some stocks lose potential | Buy Rated: Some gains, some losses

The IC Insider’s Buy Rated seal of approval is given to a stock that we believe is a compelling buy with earnings that are strong relative to the price and strong prospects of generating high price gains within the next twelve months.

Our research is backed by published reports of the company’s performance and insights of future earnings that can be found at ICInsider.com. The final decision to buy, or not, is your personal choice.

To find published reports for a Buy Rated stock on IC Insider, please choose the category ‘Buy Rated’ under Company News or enter the company name, in full or part at ‘Search IC Insider’.