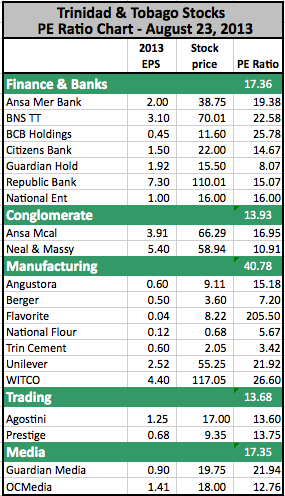

It was once said that as a country, Trinidad wanted to be the financial capital of the Caribbean, but recent activity on the country’s capital market indicates that they have a far way to go in achieving such a goal — if that is possible.

First Citizens Bank launched the largest ever Initial Public Offering (IPO) of shares in the history of the T&T Stock Exchange with a market value of approximately TT$1.1 billion on Monday 15th July at an offer price of TT$22 per share for 48,495,665 shares. The bank said the IPO will assist in widening its capital base in order to facilitate future strategic expansion plans. The offer was slated to close on August 9 and was extended to Monday, August 12th 2013 as the 9th was a public holiday.

First Citizens Brokerage & Advisory Services, a subsidiary of First Citizens Investment Services, is the Lead Broker for the Offer for Sale. The handling of the entire issue is a classic demonstration of poor investor relations and that is not a good sign for investors.

Listing on September 16 | The T&T Stock Exchange has advised that First Citizens has applied to have its shares listed on the TTSE on September 16th 2013 subject to the approval of its application to list by the Board of the TTSE.

Listing on September 16 | The T&T Stock Exchange has advised that First Citizens has applied to have its shares listed on the TTSE on September 16th 2013 subject to the approval of its application to list by the Board of the TTSE.

This is madness and is reflective of lack of sensitivity in their financial market. First off, the opening time for the issue was unnecessarily long so those who applied early had their funds tied up without any compensation. Even worse is after nearly a month of closing of the issue, investors are yet to know what is their allocation of shares. First Citizens said on their website that investors will find out between August 30 and September 6.

A check with the T&T Stock Exchange as to why it will take such a long time for the shares to be listed indicates that the problem is not with the Exchange, who are ready to list as soon the information is available and is approved by the Stock Exchange Council. A Stock Exchange source suggests that the delays maybe due to the broking community not being fully conversant with how to execute a timely IPO.

Oversubscription | Information obtained suggests that the issue was about two times oversubscribed with institutional investors probably being the main subscribers resulting in the high level of oversubscription.

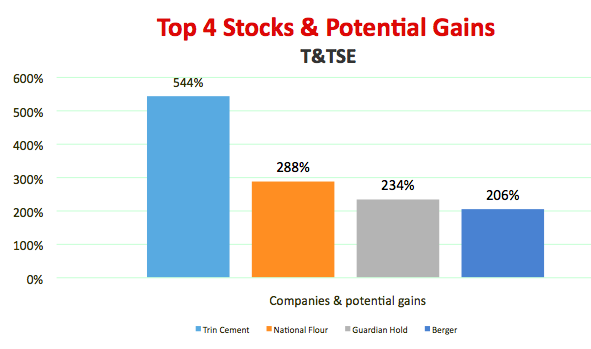

While the management has made major missteps in dealing with this issue, IC Insider still rates the stock as Buy Rated based on the issue price and potential earnings. We believe there should be a steep appreciation in the stock’s value when it is compared with others within the financial sector.

Related Posts | First Citizens’ $1B IPO opens today | T&T Citizens Bank IPO oversubscribed | Buy Rated stock list grows