It is not always that main market stocks are more attractive buys than those in the junior market, but that is what is happening currently. Strong gains, in 2016 to end of January this year, in junior market companies, resulted in Jamaica Stock Exchange main market having stocks with better values than in the junior market.

It is not always that main market stocks are more attractive buys than those in the junior market, but that is what is happening currently. Strong gains, in 2016 to end of January this year, in junior market companies, resulted in Jamaica Stock Exchange main market having stocks with better values than in the junior market.

The end result is that unlike other years when the junior market stocks tended to outperform those of in the main market by a ratio of 2 to 1, this year could see both markets gaining roughly the same.

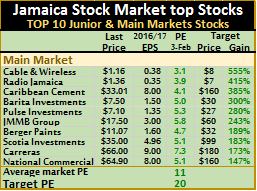

The big question, of course, is what will be the accepted PE of the market? Currently, while the average for 2016 is 17 for the main market and the ratio based on 2017 estimated earnings is 11, with 11 stocks selling above this level, Jamaica Producers and Kingston Wharves have PE ratios over 30 times 2017 earnings.

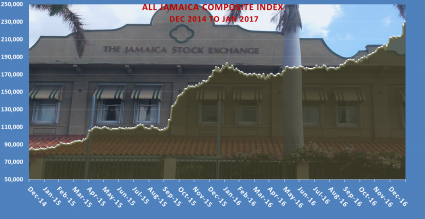

The main market faces turbulence currently as the market is sitting just below a major resistance level around 243,000 points on the All Jamaica Index. If it can overcome this level, then it will encounter resistance around the 265,000 mark.

The TOP 10 list includes 4 financial sector stocks, two communication stocks and two from the manufacturing sector.

Cable & Wireless has made considerable progress in recent years, moving from major annual losses to a stage where they reported a small profit in fiscal year 2016 to March and should break even for the nine months to December, the new financial year end. Revenues have been climbing at double digit pace and should increase even more with the upturn in economic activity and with more persons being employed. The company recently raised rates on a number of its services that should help move revenues upwards. They have also made considerable recovery in their cellular customer base and have expanded it, generating increased revenues as a result. IC Insider.com forecast calls for a profit in 2017 with growth in 2018 as well.

Cable & Wireless has made considerable progress in recent years, moving from major annual losses to a stage where they reported a small profit in fiscal year 2016 to March and should break even for the nine months to December, the new financial year end. Revenues have been climbing at double digit pace and should increase even more with the upturn in economic activity and with more persons being employed. The company recently raised rates on a number of its services that should help move revenues upwards. They have also made considerable recovery in their cellular customer base and have expanded it, generating increased revenues as a result. IC Insider.com forecast calls for a profit in 2017 with growth in 2018 as well.

On this basis, the stock is set to make solid gains. The only factor preventing that is a strong possibility that the parent company may move with an offer for the minority shares that would place a cap on the upside.

Radio Jamaica is under selling pressure as investors ignore the fundamentals and an improving economy that could result in increased profits and growth in the stock. The merger with the Gleaner was predicated a great deal on cost cutting. The group is doing just that and should benefit from a stronger marketing team and from increased advertising as businesses augment their advertising spend.

Caribbean Cement cut cost sharply in 2016 and saw growth in local sales for the first six months. However, closure of the plant for upgrading resulted in lost sales in the third quarter but sales recovered in the fourth quarter. Going into 2017, the cost savings should reduce operating cost and boost gross profit margins. Increased economic activity and lower cost of capital is leading to an uptick in the construction sector and consequently, an increase in demand for cement. The stock remains highly undervalued and has room for major gains ahead.

Barita is one of the top IC Insider’s stock for growth over the next 12 months in the main market.

Pulse Investments reported earnings of $1.35 last year and 32 cents for the September quarter that places the stock in the undervalued category even as the price climbed to $7.10 recently. It could go higher, but a bit of the earnings flow from revaluation surplus on property and that may cause some investors to discount the earnings. In a very bullish market, that may not matter much, for many investors. One positive, is that the cash flow statement shows cash inflows growing at a much higher level than in 2015.

Keith Duncan, Group Chief Executive Officer of JMMB.

Berger Paints had a very good run to December last year, with strong gains in profit as revenues grew attractively. Growth should continue into 2018 fiscal year, helped by increased building activity and an improving economy. Dividend payment should be high, thus boosting yields.

Scotia Investments should benefit in much the same way as Barita Investments. The investment bank reported earnings of $1.27 for the October quarter and IC Insider.com forecast is $4.96 for 2017. The increase should benefit from widening net interest income, as interest rates soften and more funds generated are added to the pool of interest earning pool as well as from growth in unit trust funds that will engender higher fee income, in addition to robust stock market activities that will also enhance fee income for the brokerage arm. On the negative side, the revaluation now taking place in the local currency could negatively affect earnings from trading in this area.

Carreras is one of the few stocks that have languished at the old price while many others have recorded active gains. The company just announced an interim payment of $2.20 bringing the payment since August last year to $5.40. The full year’s amount is likely to be in the order of $7.60 for a yield on the current price of 11.5 percent. This yield will not last as investors are going to eventually push it downward by bidding the price up as an income substitute. IC Insider’s forecast

is for earnings of $9 per share for the 2018 fiscal year. The stock may well languish at current levels for a while. The longer it stays the better for those investors who may want to add it to their portfolio.

is for earnings of $9 per share for the 2018 fiscal year. The stock may well languish at current levels for a while. The longer it stays the better for those investors who may want to add it to their portfolio.National Commercial Bank reported impressive profit results for their December quarter with a jump of 49 percent to $3.56 billion with earnings per share ending at $1.45, up from 96 cents in 2016. IC Insider.com forecast earnings of $8 per share for the current year. NCB declared an increase in its interim dividend payment from 50 cents in 2016 to 60 cents per ordinary stock unit payable in February. The payment represents 42.76 percent of the first quarter profits and is an indication of future payment.

Persons associated with this article may have an interest in the companies commented on.