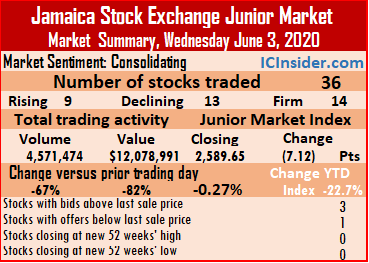

Trading on the Junior Market of the Jamaica Stock Exchange closed on Wednesday with 36 securities changing hands, resulting in an exchange of 4,571,474 units valued at $12,078,991 compared to 12,626,886 units valued at $37,770,740 from 36 stocks on Tuesday.

At the close of market activities, the prices of 9 securities advanced, 12 declined and 14 remained unchanged. The Junior Market Index declined by 7.12 points to close at 2,589.65.

At the close of market activities, the prices of 9 securities advanced, 12 declined and 14 remained unchanged. The Junior Market Index declined by 7.12 points to close at 2,589.65.

The average security traded for the day ended at 126,985 units and $335,528, in contrast to 350,747 units for an average of $1,049,187 on Tuesday. The average volume and value for the month to date amount 289,692 units valued at $1,086,852 and previously 372,181 units valued at $1,467,806. Trading in May closed with an average of 150,274 units valued at $491,077 for each security traded.

IC bid-offer Indicator| At the end of trading, the Investor’s Choice bid-offer indicator reading shows three stocks ending with bids higher than their last selling prices and one with a lower offer.

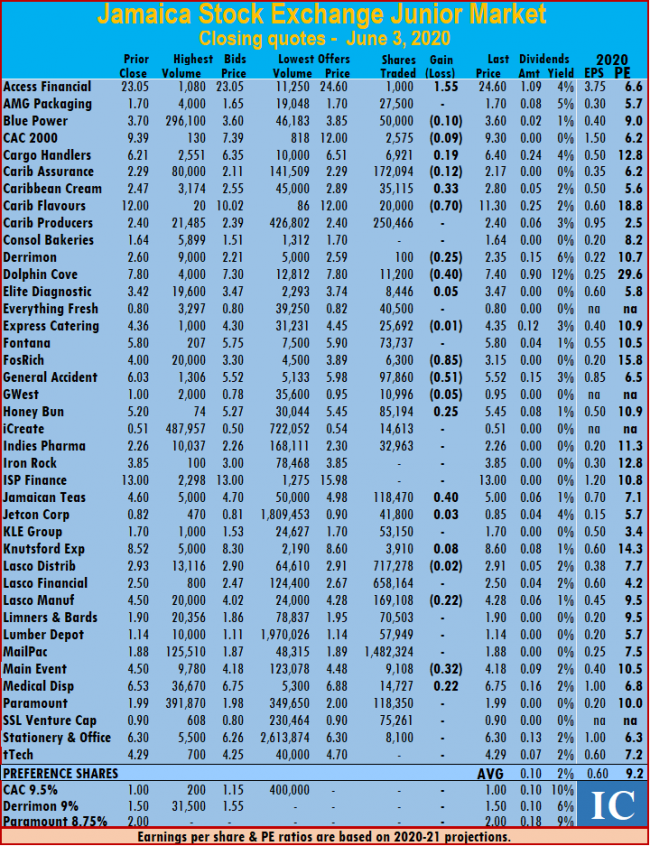

At the close of the market, Access Financial climbed $1.55 to settle at $24.60 with 1,000 shares changing hands,  Blue Power closed with a loss of 10 cents at $3.60, with an exchange of 50,000 shares, CAC 2000 declined by 9 cents in trading of 2,575 units at $9.30. Cargo Handlers ended trading with 6,921 shares, after rising 19 cents to close at $6.40, Caribbean Cream ended t with 35,115 shares changing hands after rising 33 cents to settle at $2.80. Caribbean Flavours fell 70 cents in exchanging 20,000 shares to close at $11.30, Derrimon Trading dipped 25 cents in trading of 100 units at $2.35, Dolphin Cove fell 40 cents with 11,200 units changing hands at $7.40. Elite Diagnostic closed trading of 8,446 units and gained 5 cents to end at $3.47, Express Catering ended with a loss of 1 cent at $4.35 with 25,692 stock units changing hands, Fosrich closed with a loss of 85 cents at $3.15 swapping 6,300 shares. General Accident lost 51 cents in trading of 97,860 units at $5.52, GWest Corporation exchanged 10,996 shares to close at 95 cents, after falling 5 cents, Honey Bun climbed 25 cents and exchanged 85,194 shares at $5.45.

Blue Power closed with a loss of 10 cents at $3.60, with an exchange of 50,000 shares, CAC 2000 declined by 9 cents in trading of 2,575 units at $9.30. Cargo Handlers ended trading with 6,921 shares, after rising 19 cents to close at $6.40, Caribbean Cream ended t with 35,115 shares changing hands after rising 33 cents to settle at $2.80. Caribbean Flavours fell 70 cents in exchanging 20,000 shares to close at $11.30, Derrimon Trading dipped 25 cents in trading of 100 units at $2.35, Dolphin Cove fell 40 cents with 11,200 units changing hands at $7.40. Elite Diagnostic closed trading of 8,446 units and gained 5 cents to end at $3.47, Express Catering ended with a loss of 1 cent at $4.35 with 25,692 stock units changing hands, Fosrich closed with a loss of 85 cents at $3.15 swapping 6,300 shares. General Accident lost 51 cents in trading of 97,860 units at $5.52, GWest Corporation exchanged 10,996 shares to close at 95 cents, after falling 5 cents, Honey Bun climbed 25 cents and exchanged 85,194 shares at $5.45.  Jamaican Teas ended trading with 118,470 shares, after rising 40 cents to end at $5, Jetcon Corporation closed 3 cents higher at 85 cents, with 41,800 stock units trading, Knutsford Express closed 8 cents higher at $8.60, trading 3,910 stock units. Lasco Distributors lost 2 cents with 717,278 shares changing hands to close at $2.91, Lasco Manufacturing declined by 22 cents in trading of 169,108 units at $4.28, Main Event lost 32 cents in ending at $4.18 while exchanging 9,108 shares and Medical Disposables climbed 22 cents and traded 14,727 shares at $6.75.

Jamaican Teas ended trading with 118,470 shares, after rising 40 cents to end at $5, Jetcon Corporation closed 3 cents higher at 85 cents, with 41,800 stock units trading, Knutsford Express closed 8 cents higher at $8.60, trading 3,910 stock units. Lasco Distributors lost 2 cents with 717,278 shares changing hands to close at $2.91, Lasco Manufacturing declined by 22 cents in trading of 169,108 units at $4.28, Main Event lost 32 cents in ending at $4.18 while exchanging 9,108 shares and Medical Disposables climbed 22 cents and traded 14,727 shares at $6.75.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

The market index jumped in the first 30 minutes of trading to 2,666.21 but could not hold on to the gains as it slipped back to end with a loss of 20.92 points at 2,596.77. The market closed with the average PE ratio of 9.4 times IC Insider.com projected 2020-21 earnings.

The market index jumped in the first 30 minutes of trading to 2,666.21 but could not hold on to the gains as it slipped back to end with a loss of 20.92 points at 2,596.77. The market closed with the average PE ratio of 9.4 times IC Insider.com projected 2020-21 earnings. At the close of the market, AMG Packaging exchanged 12,452 units and gained 9 cents to end at $1.70, Blue Power climbed 10 cents to $3.70 with 5,000 shares changing hands, Caribbean Cream lost 28 cents in trading 157,448 shares to close at 2.47 cents. Caribbean Flavours jumped 70 cents to $12 and exchanged 214 shares, Derrimon Trading swapped 48,300 units and gained 28 cents to end at $2.60, Elite Diagnostic closed 2 cents higher at $3.42, trading 78,926 stock units. Everything Fresh ended at 80 cents after swapping 27,139 shares and rising 5 cents, Express Catering lost 4 cents trading 61,977 shares to close at 4.36 cents, General Accident fell 2 cents in the exchange of 1,242,006 units to settle at $6.03. GWest Corporation climbed 13 cents and traded just 20 shares to finish at $1, Honey Bun fell 20 cents to 5.20 with 69,778 changing hands cents, iCreate shed 4 cents in swapping 201,238 units to close at $0.51. Indies Pharma traded 108,120 shares, after rising 1 cent to end at $2.26, Jamaican Teas lost 3 cents in the exchange of 24,648 units to close at $4.60, Jetcon Corporation swapped 3,010,893 units to finish at 82 after falling 7 cents$0.

At the close of the market, AMG Packaging exchanged 12,452 units and gained 9 cents to end at $1.70, Blue Power climbed 10 cents to $3.70 with 5,000 shares changing hands, Caribbean Cream lost 28 cents in trading 157,448 shares to close at 2.47 cents. Caribbean Flavours jumped 70 cents to $12 and exchanged 214 shares, Derrimon Trading swapped 48,300 units and gained 28 cents to end at $2.60, Elite Diagnostic closed 2 cents higher at $3.42, trading 78,926 stock units. Everything Fresh ended at 80 cents after swapping 27,139 shares and rising 5 cents, Express Catering lost 4 cents trading 61,977 shares to close at 4.36 cents, General Accident fell 2 cents in the exchange of 1,242,006 units to settle at $6.03. GWest Corporation climbed 13 cents and traded just 20 shares to finish at $1, Honey Bun fell 20 cents to 5.20 with 69,778 changing hands cents, iCreate shed 4 cents in swapping 201,238 units to close at $0.51. Indies Pharma traded 108,120 shares, after rising 1 cent to end at $2.26, Jamaican Teas lost 3 cents in the exchange of 24,648 units to close at $4.60, Jetcon Corporation swapped 3,010,893 units to finish at 82 after falling 7 cents$0.  Knutsford Express ended with 372,439 shares changing hands, after rising 11 cents to settle at $8.52, Lasco Distributors declined by 17 cents to $2.93 with an exchange of 1,534,284 units, Lasco Manufacturing shed 29 cents and traded 969,317 shares to close at $4.50. Limners and Bards ended at $1.90 after rising 7 cents and transferring 35,164 stock units, Lumber Depot inched 1 higher to $1.14, trading 76,135 shares, MailPac Group closed at $1.88, having gained 2 cents and swapping 192,266 units. Medical Disposables dropped 36 cents to settle at $6.53 with 50,350 stock units traded, Paramount Trading exchanged 461,541 shares and gained 1 cent to end at $1.99, SSL Venture climbed 15 cents and swapped 300 units to finish at 90 cents and tTech closed with a loss of 41 cents at $4.29 with 2,098 shares crossing the exchange.

Knutsford Express ended with 372,439 shares changing hands, after rising 11 cents to settle at $8.52, Lasco Distributors declined by 17 cents to $2.93 with an exchange of 1,534,284 units, Lasco Manufacturing shed 29 cents and traded 969,317 shares to close at $4.50. Limners and Bards ended at $1.90 after rising 7 cents and transferring 35,164 stock units, Lumber Depot inched 1 higher to $1.14, trading 76,135 shares, MailPac Group closed at $1.88, having gained 2 cents and swapping 192,266 units. Medical Disposables dropped 36 cents to settle at $6.53 with 50,350 stock units traded, Paramount Trading exchanged 461,541 shares and gained 1 cent to end at $1.99, SSL Venture climbed 15 cents and swapped 300 units to finish at 90 cents and tTech closed with a loss of 41 cents at $4.29 with 2,098 shares crossing the exchange. In contrast to Monday’s high volume, just 4,090,696 units valued at $13,986,258 changed hands from 31 securities on Friday.

In contrast to Monday’s high volume, just 4,090,696 units valued at $13,986,258 changed hands from 31 securities on Friday. At the close of the market, Access Financial climbed 5 cents to $23.05 with 1,242,213 shares trading, AMG Packaging ended at $1.61 after rising 6 cents and swapping 19,611 stock units, Cargo Handlers rose 16 cents in the exchange of 189,409 units to finish at $6.21. Caribbean Assurance Brokers slipped 1 cent and traded 54,706 stock units to close at $2.29, Caribbean Cream fell 9 cents to $2.75 with 272,900 shares changing hands, Caribbean Flavours jumped by $1.30 to close at $11.30 with the swapping of 2,152 stock units. Caribbean Producers gained 4 cents and exchanged 328,436 stocks to settle at $2.40, Derrimon Trading dropped 28 cents to end at $2.32 with 3,285,500 shares changing hands, Dolphin Cove closed trading of 1,100 stock units and gained 55 cents to end at $7.80. Elite Diagnostic lost 10 cents in the exchange of 7,191 units to finish at $3.40, Everything Fresh closed 2 cents higher at 75 cents with 21,000 shares traded, Express Catering settled at $4.40 after losing 5 cents and swapping 77,382 stock units. Fontana shed 14 cents in exchange of 150,506 shares to end at $5.80, General Accident traded 605,700 units and fell 20 cents to close at $6.05, Honey Bun climbed 28 cents exchanging 38,480 shares to finish at $5.40. Jamaican Teas exchanged 2,762,864 units and lost 7 cents to close at $4.63, Jetcon Corporation slipped 1 cent to 89 cents with 3,033 stock units changing hands,

At the close of the market, Access Financial climbed 5 cents to $23.05 with 1,242,213 shares trading, AMG Packaging ended at $1.61 after rising 6 cents and swapping 19,611 stock units, Cargo Handlers rose 16 cents in the exchange of 189,409 units to finish at $6.21. Caribbean Assurance Brokers slipped 1 cent and traded 54,706 stock units to close at $2.29, Caribbean Cream fell 9 cents to $2.75 with 272,900 shares changing hands, Caribbean Flavours jumped by $1.30 to close at $11.30 with the swapping of 2,152 stock units. Caribbean Producers gained 4 cents and exchanged 328,436 stocks to settle at $2.40, Derrimon Trading dropped 28 cents to end at $2.32 with 3,285,500 shares changing hands, Dolphin Cove closed trading of 1,100 stock units and gained 55 cents to end at $7.80. Elite Diagnostic lost 10 cents in the exchange of 7,191 units to finish at $3.40, Everything Fresh closed 2 cents higher at 75 cents with 21,000 shares traded, Express Catering settled at $4.40 after losing 5 cents and swapping 77,382 stock units. Fontana shed 14 cents in exchange of 150,506 shares to end at $5.80, General Accident traded 605,700 units and fell 20 cents to close at $6.05, Honey Bun climbed 28 cents exchanging 38,480 shares to finish at $5.40. Jamaican Teas exchanged 2,762,864 units and lost 7 cents to close at $4.63, Jetcon Corporation slipped 1 cent to 89 cents with 3,033 stock units changing hands,  Knutsford Express closed with a loss of 54 cents at $8.41 in the swapping of 100 shares. Lasco Distributors climbed 15 cents and exchanged 983,238 stock units to end at $3.10, Lasco Financial fell 20 cents in the trading 523,159 units to finish at $2.50, Lasco Manufacturing ended market activity at $4.79 after exchanging 91,830 shares and falling 11 cents. Limners and Bards slid 1 cent to $1.83 with 59,463 units changing hands, Lumber Depot exchanged 2,136,838 stock units after losing 1 cent to close at $1.13, Medical Disposables dipped 1 cent to $6.89 with 23,450 shares traded. Paramount Trading ended 1 cent lower at $1.98 with 38,130 stock units changing hands and Stationery and Office Supplies climbed 9 cents to $6.30 with 35,953 crossing the exchange.

Knutsford Express closed with a loss of 54 cents at $8.41 in the swapping of 100 shares. Lasco Distributors climbed 15 cents and exchanged 983,238 stock units to end at $3.10, Lasco Financial fell 20 cents in the trading 523,159 units to finish at $2.50, Lasco Manufacturing ended market activity at $4.79 after exchanging 91,830 shares and falling 11 cents. Limners and Bards slid 1 cent to $1.83 with 59,463 units changing hands, Lumber Depot exchanged 2,136,838 stock units after losing 1 cent to close at $1.13, Medical Disposables dipped 1 cent to $6.89 with 23,450 shares traded. Paramount Trading ended 1 cent lower at $1.98 with 38,130 stock units changing hands and Stationery and Office Supplies climbed 9 cents to $6.30 with 35,953 crossing the exchange. At the close of market activities, the prices of 13 securities advanced, 10 declined and eight remained unchanged. The Junior Market Index advanced by 4.54 points to close at 2,632.97 and the average PE ratio of the market ended at 9.5 times 2020-21 earnings.

At the close of market activities, the prices of 13 securities advanced, 10 declined and eight remained unchanged. The Junior Market Index advanced by 4.54 points to close at 2,632.97 and the average PE ratio of the market ended at 9.5 times 2020-21 earnings.

Knutsford Express ended at $8.95, after rising $1.45 and trading 20,792 shares, Lasco Distributors closed with a loss of 20 cents at $2.95 after swapping 92,095 shares, Lasco Manufacturing closed trading of 1,186,538 shares and gained 40 cents to end at $4.90 (See note at the foot of this story). Limners and Bards rose 2 cents and exchanged 34,476 shares at $1.84. Mailpac Group closed with a loss of 2 cents at $1.86while trading 792,156 shares, Medical Disposables ended market activity, exchanging 4,114 stock units to settle at $6.90 after falling 10 cents and Stationery and Office Supplies lost 6 cents in trading 97,229 shares at $6.21.

Knutsford Express ended at $8.95, after rising $1.45 and trading 20,792 shares, Lasco Distributors closed with a loss of 20 cents at $2.95 after swapping 92,095 shares, Lasco Manufacturing closed trading of 1,186,538 shares and gained 40 cents to end at $4.90 (See note at the foot of this story). Limners and Bards rose 2 cents and exchanged 34,476 shares at $1.84. Mailpac Group closed with a loss of 2 cents at $1.86while trading 792,156 shares, Medical Disposables ended market activity, exchanging 4,114 stock units to settle at $6.90 after falling 10 cents and Stationery and Office Supplies lost 6 cents in trading 97,229 shares at $6.21. At the end of market activities on Thursday, 29 securities changing hands, with the prices of 12 securities advanced, 12 declined and five remained unchanged. The PE ratio of the market ended at 9.3 times 2020-21 earnings.

At the end of market activities on Thursday, 29 securities changing hands, with the prices of 12 securities advanced, 12 declined and five remained unchanged. The PE ratio of the market ended at 9.3 times 2020-21 earnings. At the close of the market, Access Financial shed 49 cents in trading of 1,000 units to settle at $22.51, AMG Packaging declined by 25 cents to $1.50 with 2,200 units changing hands,

At the close of the market, Access Financial shed 49 cents in trading of 1,000 units to settle at $22.51, AMG Packaging declined by 25 cents to $1.50 with 2,200 units changing hands,  Jetcon Corporation fell 9 cents and closed at 80 cents after swapping 50,000 shares.

Jetcon Corporation fell 9 cents and closed at 80 cents after swapping 50,000 shares.

At the close of the market, Access Financial shed 25 cents in the exchange of 47,605 units to end at $23, Caribbean Assurance Brokers fell 15 cents to $2.30 with 5,834 shares changing hands, Caribbean Cream slipped 3 cents and traded 4,900 shares to close at $2.72. Caribbean Flavours ended 2 cents lower at $10 in an exchange of 1,276,041 stock units, Derrimon Trading declined by 22 cents and exchanged 211,000 shares to settle at $2.50, Dolphin Cove rose by 25 cents to $7.25 in swapping 1,545 units. Elite Diagnostic ended at $3.35 after falling 5 cents and trading 24,942 shares, Everything Fresh declined by 5 cents in the swapping of 116,123 stock units to close at 75 cents, Express Catering leaped 99 cents to $4.51 in the exchange of 29,558 shares. Fontana closed at $5.95 after climbing 35 cents and trading 507,948 stock units, Fosrich fell 15 cents in the trade of 11,795 units to close at $3.85,

At the close of the market, Access Financial shed 25 cents in the exchange of 47,605 units to end at $23, Caribbean Assurance Brokers fell 15 cents to $2.30 with 5,834 shares changing hands, Caribbean Cream slipped 3 cents and traded 4,900 shares to close at $2.72. Caribbean Flavours ended 2 cents lower at $10 in an exchange of 1,276,041 stock units, Derrimon Trading declined by 22 cents and exchanged 211,000 shares to settle at $2.50, Dolphin Cove rose by 25 cents to $7.25 in swapping 1,545 units. Elite Diagnostic ended at $3.35 after falling 5 cents and trading 24,942 shares, Everything Fresh declined by 5 cents in the swapping of 116,123 stock units to close at 75 cents, Express Catering leaped 99 cents to $4.51 in the exchange of 29,558 shares. Fontana closed at $5.95 after climbing 35 cents and trading 507,948 stock units, Fosrich fell 15 cents in the trade of 11,795 units to close at $3.85,  Knutsford Express jumped 28 cents to $8.98 with 36,752 units changing hands. Lasco Distributors dropped 17 cents to $2.73, with 34,238 shares crossing the exchange, Lasco Financial slipped 5 cents and exchanged 198,900 shares to end at $2.65, Lasco Manufacturing traded a volume leading 6,099,978 units to close at $4.01 after inching 1 cent higher. Limners and Bards increased by 20 cents in swapping 410,000 units to end at $1.95, Lumber Depot finished 1 cent lower at $1.13 with 88,045 shares changing hands,

Knutsford Express jumped 28 cents to $8.98 with 36,752 units changing hands. Lasco Distributors dropped 17 cents to $2.73, with 34,238 shares crossing the exchange, Lasco Financial slipped 5 cents and exchanged 198,900 shares to end at $2.65, Lasco Manufacturing traded a volume leading 6,099,978 units to close at $4.01 after inching 1 cent higher. Limners and Bards increased by 20 cents in swapping 410,000 units to end at $1.95, Lumber Depot finished 1 cent lower at $1.13 with 88,045 shares changing hands,  Investors traded 32 securities, resulting in an exchange of 4,137,638 units valued at $10,997,880 compared to 4,259,300 units valued at $14,475,328 from 35 securities on Friday. The average PE ratio of the Junior Market ended at 9.2 based on 2020-21 earnings.

Investors traded 32 securities, resulting in an exchange of 4,137,638 units valued at $10,997,880 compared to 4,259,300 units valued at $14,475,328 from 35 securities on Friday. The average PE ratio of the Junior Market ended at 9.2 based on 2020-21 earnings. At the close of the market, Cargo Handlers dropped 50 cents to $6.05 with 6,438 units traded, Caribbean Cream closed 6 cents higher at $2.75 with an exchange of 61,233 stock units, Caribbean Producers traded 1,418,225 shares and fell 12 cents to end at $2.40. Derrimon Trading jumped 22 cents in swapping of 28,295 shares to settle at $2.72, Dolphin Cove shed 23 cents to close at $7 with 5,709 units changing hands, Elite Diagnostic gained 11 cents and exchanged 92,470 shares to settle at $3.40. Express Catering inched 1 cent higher to finish at $3.52 with 33,230 units traded, Fontana dropped 30 cents to $5.60 with 220,601 units crossing the market, General Accident leaped 49 cents exchanging 30,026 stock units to close at $6.50. GWest lost 3 cents in the trading of 1,160 shares to close at 87 cents, Honey Bun declined by 37 cents to $5.08 with 131,812 shares changing hands, iCreate closed 3 cents lower at 52 cents with 87,177 stock units traded. Indies Pharma picked up 2 cents and exchanged 13,245 shares to settle at $2.22, Iron Rock Insurance ended the day 10 cents down, at $3.80 with an exchange of 10,000 shares,

At the close of the market, Cargo Handlers dropped 50 cents to $6.05 with 6,438 units traded, Caribbean Cream closed 6 cents higher at $2.75 with an exchange of 61,233 stock units, Caribbean Producers traded 1,418,225 shares and fell 12 cents to end at $2.40. Derrimon Trading jumped 22 cents in swapping of 28,295 shares to settle at $2.72, Dolphin Cove shed 23 cents to close at $7 with 5,709 units changing hands, Elite Diagnostic gained 11 cents and exchanged 92,470 shares to settle at $3.40. Express Catering inched 1 cent higher to finish at $3.52 with 33,230 units traded, Fontana dropped 30 cents to $5.60 with 220,601 units crossing the market, General Accident leaped 49 cents exchanging 30,026 stock units to close at $6.50. GWest lost 3 cents in the trading of 1,160 shares to close at 87 cents, Honey Bun declined by 37 cents to $5.08 with 131,812 shares changing hands, iCreate closed 3 cents lower at 52 cents with 87,177 stock units traded. Indies Pharma picked up 2 cents and exchanged 13,245 shares to settle at $2.22, Iron Rock Insurance ended the day 10 cents down, at $3.80 with an exchange of 10,000 shares,  Jamaican Teas climbed 6 cents to settle at $4.35 with 158,546 units crossing the market. Limners and Bards dipped 7 cents to $1.75 with 103,494 shares traded, Lumber Depot swapped 136,889 shares to finish at $1.14 after gaining 2cents, Medical Disposables jumped 30 cents to $7.30 with an exchange of 21,814 units. Paramount Trading added 1 cent to finish at $2 after trading 12,300 shares and Stationery and Office Supplies closed 25 cents higher at $6.25, with 5,809 stock units crossing the exchange.

Jamaican Teas climbed 6 cents to settle at $4.35 with 158,546 units crossing the market. Limners and Bards dipped 7 cents to $1.75 with 103,494 shares traded, Lumber Depot swapped 136,889 shares to finish at $1.14 after gaining 2cents, Medical Disposables jumped 30 cents to $7.30 with an exchange of 21,814 units. Paramount Trading added 1 cent to finish at $2 after trading 12,300 shares and Stationery and Office Supplies closed 25 cents higher at $6.25, with 5,809 stock units crossing the exchange.

Cargo Handlers closed 5 cents higher at $6.55, with 190 stock units trading, Caribbean Cream climbed 15 cents and exchanged 734 shares at $2.69, Caribbean Producers closed 11 cents higher at $2.52, with 477,643 stock units trading. Derrimon Trading closed 7 cents higher at $2.50, with 17,431 stock units traded, Elite Diagnostic declined by 59 cents in exchanging 9,360 units at $3.29, Express Catering climbed 16 cents and exchanged 18,269 shares at $3.51, Fosrich closed 30 cents higher after trading 99,267 stock units at $4. Fontana closed trading of 96,620 units and gained 34 cents to end at $5.90, General Accident closed 2 cents higher at $6.01, with 648,867 stock units trading. Honey Bun climbed 45 cents and exchanged 52,137 shares at $5.45, iCreate closed with 112,094 units passing through the market and gained 2 cents to end at 55 cents, Iron Rock Insurance declined by 9 cents to settle at $3.90, with 3,000 units changing hands. Jamaican Teas ended trading of 125,687 units with gains of 39 cents to end at $4.29, Jetcon Corporation closed with a loss of 8 cents at 80 cents swapping 28,000 shares, Knutsford Express closed trading of 500 units and gained 20 cents to end at $8.70.

Cargo Handlers closed 5 cents higher at $6.55, with 190 stock units trading, Caribbean Cream climbed 15 cents and exchanged 734 shares at $2.69, Caribbean Producers closed 11 cents higher at $2.52, with 477,643 stock units trading. Derrimon Trading closed 7 cents higher at $2.50, with 17,431 stock units traded, Elite Diagnostic declined by 59 cents in exchanging 9,360 units at $3.29, Express Catering climbed 16 cents and exchanged 18,269 shares at $3.51, Fosrich closed 30 cents higher after trading 99,267 stock units at $4. Fontana closed trading of 96,620 units and gained 34 cents to end at $5.90, General Accident closed 2 cents higher at $6.01, with 648,867 stock units trading. Honey Bun climbed 45 cents and exchanged 52,137 shares at $5.45, iCreate closed with 112,094 units passing through the market and gained 2 cents to end at 55 cents, Iron Rock Insurance declined by 9 cents to settle at $3.90, with 3,000 units changing hands. Jamaican Teas ended trading of 125,687 units with gains of 39 cents to end at $4.29, Jetcon Corporation closed with a loss of 8 cents at 80 cents swapping 28,000 shares, Knutsford Express closed trading of 500 units and gained 20 cents to end at $8.70.  Lasco Distributors declined by 10 cents trading 630,500 units at $2.90, Lasco Manufacturing fell by 30 cents exchanging 797,613 units at $4, Limners and Bards dipped 8 cents trading 198,771 units at $1.82. Lumber Depot shed 2 cents trading 370,242 units at $1.12, MailPac Group closed with a loss of 3 cents at $1.88 swapping 251,508 shares, Medical Disposables shed 5 cents transferring 22,711 units at $7. Main Event lost 10 cents in trading of 18,000 units at $4.08, Stationery and Office Supplies lost 5 cents 20,757 units changing hands at $6. SSL Venture ended market activity while exchanging 18,400 shares to close at 75 cents, after falling 10 cents and tTech closed with a loss of 9 cents at $4.41 after swapping 42,269 shares.

Lasco Distributors declined by 10 cents trading 630,500 units at $2.90, Lasco Manufacturing fell by 30 cents exchanging 797,613 units at $4, Limners and Bards dipped 8 cents trading 198,771 units at $1.82. Lumber Depot shed 2 cents trading 370,242 units at $1.12, MailPac Group closed with a loss of 3 cents at $1.88 swapping 251,508 shares, Medical Disposables shed 5 cents transferring 22,711 units at $7. Main Event lost 10 cents in trading of 18,000 units at $4.08, Stationery and Office Supplies lost 5 cents 20,757 units changing hands at $6. SSL Venture ended market activity while exchanging 18,400 shares to close at 75 cents, after falling 10 cents and tTech closed with a loss of 9 cents at $4.41 after swapping 42,269 shares. At the close of the market, the recently listed Caribbean Assurance Brokers climbed 11 cents to $2.50 with an exchange of 80,524 units as supply continues to dry up for the stock. Caribbean Cream ended with a loss of 1 cent at $2.54 with 20,000 stock units changing hands, Caribbean Producers finished at $2.41 after sliding 8 cents in the swapping 526,391 units, Derrimon Trading jumped 31 cents in the exchange of 85,106 shares to close at $2.43. Everything Fresh ended 9 cents higher at 80 cents with 26,000 shares changing hands, Express Catering shed 16 cents trading 23,200 stock units at $3.35, Fontana ended market activity 12 cents higher at $5.56 trading 298,168 shares. General Accident jumped 99 cents in the exchange of 1,404,778 units to close at $5.99 after the company posted first-quarter results, with profit rising 146 percent to $76 million as investments and other income grew from just $7 million to $74 million. Honey Bun fell 15 cents to $5 with 34,711 shares crossing the exchange, iCreate added 2 cents and exchanged 70,302 shares to finish at 53 cents, Iron Rock Insurance climbed 54 cents to $3.99 with trading a mere 200 units, Jamaican Teas lost 10 cents in swapping 41,176 units to end at $3.90.

At the close of the market, the recently listed Caribbean Assurance Brokers climbed 11 cents to $2.50 with an exchange of 80,524 units as supply continues to dry up for the stock. Caribbean Cream ended with a loss of 1 cent at $2.54 with 20,000 stock units changing hands, Caribbean Producers finished at $2.41 after sliding 8 cents in the swapping 526,391 units, Derrimon Trading jumped 31 cents in the exchange of 85,106 shares to close at $2.43. Everything Fresh ended 9 cents higher at 80 cents with 26,000 shares changing hands, Express Catering shed 16 cents trading 23,200 stock units at $3.35, Fontana ended market activity 12 cents higher at $5.56 trading 298,168 shares. General Accident jumped 99 cents in the exchange of 1,404,778 units to close at $5.99 after the company posted first-quarter results, with profit rising 146 percent to $76 million as investments and other income grew from just $7 million to $74 million. Honey Bun fell 15 cents to $5 with 34,711 shares crossing the exchange, iCreate added 2 cents and exchanged 70,302 shares to finish at 53 cents, Iron Rock Insurance climbed 54 cents to $3.99 with trading a mere 200 units, Jamaican Teas lost 10 cents in swapping 41,176 units to end at $3.90.  Lasco Distributors declined 3 cents to finish at $3 in the trading 95,285 units, Lasco Manufacturing jumped 25 cents and swapped 1,481 shares to settle at $4.30, Limners and Bards finished at $1.90 after gaining 5 cents and exchanging 12,428 shares. Lumber Depot added 1 cent and traded 79,678 units to close at $1.14, MailPac picked up 3 cents to end at $1.91 with 166,821 shares changing hands, Main Event rounded out the day at $4.18 after gaining 10 cents and exchanging 200 shares. Medical Disposables closed trading of 77,337 units and slipped 7 cents to end at $7.05, Stationery and Office Supplies dropped 25 cents in swapping 68,787 shares to settle at $6.05 and tTech fell 25 cents to $4.50 with 21,000 with units crossing the exchange.

Lasco Distributors declined 3 cents to finish at $3 in the trading 95,285 units, Lasco Manufacturing jumped 25 cents and swapped 1,481 shares to settle at $4.30, Limners and Bards finished at $1.90 after gaining 5 cents and exchanging 12,428 shares. Lumber Depot added 1 cent and traded 79,678 units to close at $1.14, MailPac picked up 3 cents to end at $1.91 with 166,821 shares changing hands, Main Event rounded out the day at $4.18 after gaining 10 cents and exchanging 200 shares. Medical Disposables closed trading of 77,337 units and slipped 7 cents to end at $7.05, Stationery and Office Supplies dropped 25 cents in swapping 68,787 shares to settle at $6.05 and tTech fell 25 cents to $4.50 with 21,000 with units crossing the exchange. The day’s activities ended with 30 securities changing hands, resulting in an exchange of 2,553,437 units valued at $9,523,569 compared to 7,713,659 units for $39,344,491 from 31 companies on Tuesday. The average PE ratio of the Junior Market ended at 9.1 times 2020-21 earnings.

The day’s activities ended with 30 securities changing hands, resulting in an exchange of 2,553,437 units valued at $9,523,569 compared to 7,713,659 units for $39,344,491 from 31 companies on Tuesday. The average PE ratio of the Junior Market ended at 9.1 times 2020-21 earnings. IC bid-offer Indicator| At the end of trading, the Investor’s Choice bid-offer indicator reading shows three stocks ended with bids higher than its last selling prices and three with lower offers.

IC bid-offer Indicator| At the end of trading, the Investor’s Choice bid-offer indicator reading shows three stocks ended with bids higher than its last selling prices and three with lower offers. ISP Finance shed $1.90 in the trading of 6,010 shares to end at $14, Jamaican Teas inched 1 cent higher and exchanged 52,000 shares to settle at $4, Knutsford Express jumped 80 cents to $8.50 with 3,470 units changing hands. Lasco Distributors climbed 73 cents to $3.03, with the swapping of 200 shares, Lasco Financial picked up 10 cents and exchanged 36,897 shares to end at $2.70, Lasco Manufacturing traded 1,018,392 units to close at $4.05 after slipping 4 cents. Limners and Bards declined 5 cents in switching 5,500 units to end at $1.85, Lumber Depot gained 1 cent to end at $1.13 with 95,476 shares traded, MailPac Group gained 4 cents in the exchange of 343,873 units to settle at $1.88 and Medical Disposables jumped 82 cents to close at $7.12 with 6,000 shares crossing the exchange.

ISP Finance shed $1.90 in the trading of 6,010 shares to end at $14, Jamaican Teas inched 1 cent higher and exchanged 52,000 shares to settle at $4, Knutsford Express jumped 80 cents to $8.50 with 3,470 units changing hands. Lasco Distributors climbed 73 cents to $3.03, with the swapping of 200 shares, Lasco Financial picked up 10 cents and exchanged 36,897 shares to end at $2.70, Lasco Manufacturing traded 1,018,392 units to close at $4.05 after slipping 4 cents. Limners and Bards declined 5 cents in switching 5,500 units to end at $1.85, Lumber Depot gained 1 cent to end at $1.13 with 95,476 shares traded, MailPac Group gained 4 cents in the exchange of 343,873 units to settle at $1.88 and Medical Disposables jumped 82 cents to close at $7.12 with 6,000 shares crossing the exchange.