Berger Paints is one of IC Insider.com’s top stocks for 2020. It is may not the most popular company listed on the Jamaica Stock Exchange, but it seems set to surprise many investors with its performance in 2020. ![]()

It gained much attention with strong growth in profits in the financial year to March 2017, ahead of a switch in majority ownership in August 2017 to the Trinidad based ANSA McAL Group resulting in significant changes in directorship and management. In 2019, the company changed the General manager after a relatively short stint at the helm, a move that could augur well for the company going forward.

In 2019, raw materials accounted for 50 percent of the input into paint production. Most of the raw material used in paint production is petroleum-based, resulting in paint companies benefit when the petrochemical industry goes into a downswing and conversely, a hike in the price of petroleum products raises input costs. Titanium dioxide and crude derivatives form about 50 percent of the raw material cost of paints. In 2019 the average price of crude oil on the world market US$57 for WTI, for 2020 so far, it is at US$43 per barrel, with the current price around US$22 per barrel. If the current trend holds, it will result in lower input costs for Berger for 2020. Management in reporting to shareholders for the year to December stated, “year to date to February 2020, performance indicators are ahead of 2019 with signs of a positive trajectory”.

Between 2012 and 2017, profits increased at an outstanding rate, however, in 2018, the profit was relatively flat and declined in 2019. The company reported lower sales and sharply reduced profit for 2019. The company recorded a two percent reduction in revenues to $1.12 billion for the six months to June and a 6 percent reduction to $1.6 billion for the nine months to September 2019, versus $1.7 billion for the corresponding period in 2018. It ended the year down 7 percent at $2.5 billion. Adverse weather conditions experienced in the third and fourth quarters, negatively impacted revenues, the company told shareholders in a statement accompanying the third and fourth quarter reports. Also affecting sales was the extensive road works that disrupted their customers’ businesses.

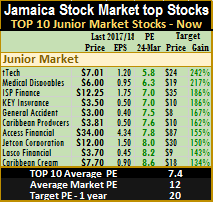

Berger Paints is one of IC Insider’s TOP 10 stocks.

“The company implemented a new an Enterprise Resource Planning Software (ERP) system which provides a fully integrated manufacturing and financial platform and is providing the required details and analytics for the business, the management stated.” The company also introduced a new automotive line of paints to deepen BPJL’s reach into the automotive market.

IC Insider.com projects earnings per share amounting to $2 for the current year and it now trades at an attractive P/E of just over six times projected earnings.

Trinidad’s

Trinidad’s  Insider trading in the stock of the company they are connected to can be a big indicators of future prospects, but it is not always the case.

Insider trading in the stock of the company they are connected to can be a big indicators of future prospects, but it is not always the case.

by

by