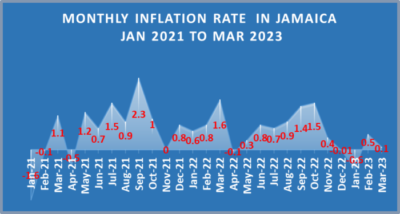

Inflation has moderated substantially since the sharp spike in 2021 and the Bank of Jamaica has some role in it, with tighter monetary policy, but the price may be much greater than may be visible currently. A look at BOJ reports on inflation since 2021 is very worrying, when compared with the actual outcome, suggesting that the MPC that is guiding the BOJ has done a terrible job in its forecasts. This is a matter the Minister of Finance must carefully look at and so correct what is clearly a major area of concern in managing a very critical part of the country’s economy.

The job of fighting high inflation may be substantially done for this round, how efficiently was it executed is another matter that the country needs to have answered. A careful look at reports emanating from the Bank of Jamaica tells a tale of what looks more like guesswork, than scholarly assessment. Don’t take our word for it, compare BOJ’s utterances since 2021 and their outturn.

The job of fighting high inflation may be substantially done for this round, how efficiently was it executed is another matter that the country needs to have answered. A careful look at reports emanating from the Bank of Jamaica tells a tale of what looks more like guesswork, than scholarly assessment. Don’t take our word for it, compare BOJ’s utterances since 2021 and their outturn.

Up to April 2021, BOJ fiddled around telling the country that inflation was well under control and that it would remain within the band of 4-6 percent for two years, that’s before they quickly found out that it was not going to be so. Even then rather than acting promptly, they waited until August to announce an increase in the overnight rate, although admittedly they started to pull money out of the market earlier by way of certificate of deposits.

Something must be terribly wrong that within a month of assuring the Minister of Finance that all will be well they had a change of mind. The same thing seems to be happening currently, with inflation set to be within, or very close to the 4-6 percent range in April well ahead of the forecast made by the BOJ at their March meeting when they stated that the target would not be reached until the fourth quarter this year.

The Governor of the Central Bank informed the Ministry of Finance in April 2021, that they could not increase interest rates as that would trim economic growth. But by May 2021, they were singing a different song of higher inflation and forecast for increased rates.

In May, last year they made an erroneous statement that inflation was still moving higher and would increase over the next two months, in fact the underlying data was suggesting that it was improving. Importantly, at their last meeting at which they reviewed the state of inflation they felt so comfortable that things were in line with their forecast that the next meeting was set for May. Had they looked at the real message that had been screaming at them for 2022 and more so since November they would have taken action to reduce overnight interest rates from then.

In May, last year they made an erroneous statement that inflation was still moving higher and would increase over the next two months, in fact the underlying data was suggesting that it was improving. Importantly, at their last meeting at which they reviewed the state of inflation they felt so comfortable that things were in line with their forecast that the next meeting was set for May. Had they looked at the real message that had been screaming at them for 2022 and more so since November they would have taken action to reduce overnight interest rates from then.

The MPC release stated, “Annual inflation is projected to continue to fall to the Bank’s inflation target range of 4.0 to 6.0 per cent by the December 2023 quarter. One-off regulated price adjustments may, however, result in a temporary uptick in inflation.”

“Notwithstanding these positive developments, the MPC noted that the risks to the inflation outlook remain elevated. In a context where the domestic economy continues to grow, labour market shortages carry the potential for future wage adjustments that can put upward pressure on inflation. Higher inflation could also result from a worsening in supply chain conditions and higher commodity prices if there are further geo-political disruptions. Among the factors that could lead to lower-than-projected inflation, weaker-than-expected global growth could negatively affect domestic demand, and some projected adjustments to regulated prices may not materialise.”

Therefore, to continue underpinning inflation returning to the target range and to underwrite continued stability in the foreign exchange market, the MPC unanimously agreed to hold the policy interest rate at 7 percent, to maintain tight Jamaican dollar liquidity in the money market and to continue fostering relative stability in the foreign exchange market. The Bank’s liquidity management strategy incorporates the impact of the one percentage point increase in the domestic and the foreign currency Cash Reserve Requirements applicable to DTIs, effective 01 April 2023.”

BOJ sucks $11 billion from money market

Bank of Jamaica sucked more money from the financial market on Wednesday, April 5, pushing the total CDs outstanding to $99 billion, up from $89 a week ago, with the average rate holding steady under 8.5 percent for a second week but the total amount of CDs outstanding is still below the record of $109.5 billion on March 1.

The bank offered $34 billion in CDs and attracted $59.7 billion from 351 bids, with only 253 successful bids getting allocated funds. The offer elicited bids as high as 13.5 percent and as low as 8 percent. The interest rate for the highest successful bid was 8.749 percent and received 75.23 percent of the amount applied for, with the highest fully satisfied rate being 8.74 percent.

The bank offered $34 billion in CDs and attracted $59.7 billion from 351 bids, with only 253 successful bids getting allocated funds. The offer elicited bids as high as 13.5 percent and as low as 8 percent. The interest rate for the highest successful bid was 8.749 percent and received 75.23 percent of the amount applied for, with the highest fully satisfied rate being 8.74 percent.

At the auction on March 29, a total of 438 bids amounting to $70 million chased after the $35 billion on offer, with 302 being successful at an average rate of 8.49 percent and resulting in $88.85 billion being quarantined by the central bank. The rate on CDs fell to an average of 8.85 at the March 22 auction from the prior auction rate of 10.54 percent.

Long term GOJ interest rates spike to 11% high

Investors garnered interest rates as high as 11 percent on long term bonds issued by the Government of Jamaica last week auctions of three long term bonds that were reopened and raised $10 billion. The average rates were more moderate, with the highest average being 8 percent.

The Government also offered $5 billion of the 10 percent bond due 2037 with a duration of 15.5 years. The auction attracted $6.759 billion that resulted in an average yield of 7.9614 percent. The lowest rate was 6.7 percent for $50 million and the highest success rate was 10 percent. The highest submitted bid was 12.999 percent. A total of 56 bids went after the bond, with 46 being successful.

The 5.675 percent bond due 2029, with a duration of 7.5 years, ended with an average yield of 6.3506 percent. The auction attracted $2.727 billion, of which $1 billion was allocated. The lowest rate was 5.575 percent for $100 million and the highest success rate was 6.94 percent. The highest submitted bid was 11 percent. This instrument received 43 submissions, with only 18 being successful.

The 4.5 percent bond due 2025, with a duration of 3.5 years, delivered an average yield of 6.2329 percent. Bids from 51 applicants amounting to $4.779 billion chased the $4 billion on offer. Only 44 bids succeeded in getting allocated. The lowest rate was 4.5 percent for $44 million, with the highest success rate of 10.525 percent. The highest submitted bid was 11 percent covering $100 million.

The increased rates come against the background of recent moves by Jamaica’s central bank to hike rates and move towards an era of positive interest rates. Since making their intention known, the bank raised its overnight rate from 0.50 percent to 2 percent in September and November, while rates on 30 days CDs moved to 4.11 percent from 0.59 percent since the beginning of August and 2.15 percent at the September 22 Auction.

Have Interest rates peaked?

Jamaica’s Central Bank

Interest rates on Certificate of Deposit issued by Bank of Jamaica seem to be levelling off, with the rate at last week’s auction declining from the previous week’s outturn.

Last week’s offer of $7.5 billion in 30 days on Wednesday, 27 October, attracted 76 applications amounting to $13 billion and resulted in an average yield of 3.96 percent, down from 4.53 percent at the auction in the previous week. Bids were received as low as 2.5 percent covering $1.48 billion, with the highest rate bid being 7.34 percent for $20 million. A bid amounting to $550 million received full allocation at 4.79 percent. The total nominal outstanding amount for the 30-day CDs on the settlement date – 29 October, will be $41.5 billion, down from $46.5 billion in mid-October.