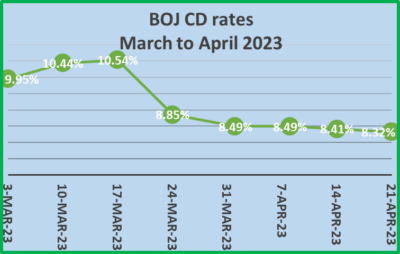

Bank of Jamaica’s latest CD offer of $20 billion attracted 186 bids amounting to $44,629,464,000, but only 75 bids were successful and resulted in the average yield of 8.32 percent for successful bids, that is down from 8.41 percent at last week’s auction and represents the fourth decline since the rates closed at 10.54 percent for the March 17 CDs.

Bank of Jamaica’s latest CD offer of $20 billion attracted 186 bids amounting to $44,629,464,000, but only 75 bids were successful and resulted in the average yield of 8.32 percent for successful bids, that is down from 8.41 percent at last week’s auction and represents the fourth decline since the rates closed at 10.54 percent for the March 17 CDs.

The lowest bid at this week’s auction was 7.50 percent, down from 8 percent last week and the highest bid was 11 percent, but the highest rate for total allocation was 8.349 percent, with the highest rate for partial allocation being 8.34999 percent resulting in success for 99.30 percent of the amount applied for.

The total nominal outstanding amount for the 30-day CDs on April 21 will be $106 billion.

More decline in interest rates

BOJ must slash the ON rate to 5% now

Bank of Jamaica must make a bold move and cut the Overnight rate they charge banks to 5 percent from 7 percent now and prevent driving the economy into recession, with inflation now within the Bank’s target range and set to fall lower over the next few months.

The cut in rates now is also essential to help pension funds and the fall in the value of many of the interest sensitive assets with the financial market that fell had to be marked down to market, with higher interest rates and impaired capital in some of the country’s banks.

The cut in rates now is also essential to help pension funds and the fall in the value of many of the interest sensitive assets with the financial market that fell had to be marked down to market, with higher interest rates and impaired capital in some of the country’s banks.

Many observers may credit BOJ with managing the inflation in Jamaica well and bringing it back to their target 4-6 percent range. The problem is that the country is now faced with severely undershooting the lower end of the target, a target this publication thinks should be revised down to 2.5 to 4 percent.

In March, ICInsdier.com published an article captioned “Time come for BOJ to cut interest rates”.

We posited that “Interest rates in Jamaica and around the world were pushed up since 2021 to curb inflation that got out of hand, in the process Bank of Jamaica hiked their overnight rate from 0.50 percent August 2021 to a high of 7 percent in November last year, since then point to point inflation peaked in April last year at 11.8 percent, but has since declined sharply by 34 percent to February this year, with the pace since November last year running at 44 percent below the 2021 period.

The average monthly inflation rate has dropped from the 2022 level of 0.6 percent per month from November 2021 to October 2022. It is now running at an average of 0.2 percent per month or 2.4 percent per annum over the last five months, well below the Bank’s target of 4-6 percent per annum.  If history is anything to go by, the next three months should see relatively low inflation, suggesting that the current average of 0.2 per month could continue for a few more months. The fall has been consistent, although the rate for a few months exceeded this pace.”

If history is anything to go by, the next three months should see relatively low inflation, suggesting that the current average of 0.2 per month could continue for a few more months. The fall has been consistent, although the rate for a few months exceeded this pace.”

Bank of Jamaica’s target of 4-6 percent is close at hand based on the point to point inflation, with the danger now that the rate could fall well below the lower end of the band if BOJ does not act soon to lower interest rates.

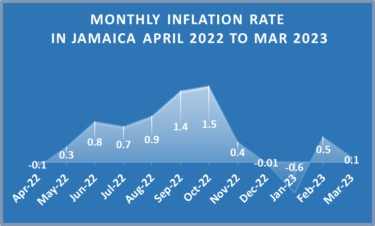

Since then, inflation has remained very low, as we forecasted, with the All-Jamaica Consumer Price Index (CPI) increasing by a mere 0.1 per cent for March 2023.

The big problem is that BOJ MPC members are constantly looking backwards at the point to point inflation and not correctly reading the more critical signals in the data they sent that inflation was killed from 2022.

BOJ sucks $11 billion from money market

Bank of Jamaica sucked more money from the financial market on Wednesday, April 5, pushing the total CDs outstanding to $99 billion, up from $89 a week ago, with the average rate holding steady under 8.5 percent for a second week but the total amount of CDs outstanding is still below the record of $109.5 billion on March 1.

The bank offered $34 billion in CDs and attracted $59.7 billion from 351 bids, with only 253 successful bids getting allocated funds. The offer elicited bids as high as 13.5 percent and as low as 8 percent. The interest rate for the highest successful bid was 8.749 percent and received 75.23 percent of the amount applied for, with the highest fully satisfied rate being 8.74 percent.

The bank offered $34 billion in CDs and attracted $59.7 billion from 351 bids, with only 253 successful bids getting allocated funds. The offer elicited bids as high as 13.5 percent and as low as 8 percent. The interest rate for the highest successful bid was 8.749 percent and received 75.23 percent of the amount applied for, with the highest fully satisfied rate being 8.74 percent.

At the auction on March 29, a total of 438 bids amounting to $70 million chased after the $35 billion on offer, with 302 being successful at an average rate of 8.49 percent and resulting in $88.85 billion being quarantined by the central bank. The rate on CDs fell to an average of 8.85 at the March 22 auction from the prior auction rate of 10.54 percent.

BOJ CD rate drop for a second week

Rates paid on Bank of Jamaica 30 days CDs dropped for a second week at the latest auction on Wednesday this week, to 8.49 percent from 8.85 percent on March 22.

The rate declined from 10.54 percent at the auction on March 17 after BOJ offered $18 billion, which attracted $57.86 billion on March 22. At this week’s auction, $35 billion was offered by the central bank and attracted $70 billion, resulting in the highest successful rate at 8.85 percent and the lowest at 7.5 percent, down from 8.2 percent the week before. BOJ absorbed $88.85 billion at the end of the CD auction, up from $81.85 billion the previous week but still down sharply from a peak at $109.5 on March 1.

The rate declined from 10.54 percent at the auction on March 17 after BOJ offered $18 billion, which attracted $57.86 billion on March 22. At this week’s auction, $35 billion was offered by the central bank and attracted $70 billion, resulting in the highest successful rate at 8.85 percent and the lowest at 7.5 percent, down from 8.2 percent the week before. BOJ absorbed $88.85 billion at the end of the CD auction, up from $81.85 billion the previous week but still down sharply from a peak at $109.5 on March 1.

The move brings the CD rates in line with Treasury bills, with an average rate for 90 days coming in at 8.21 percent on March 8.

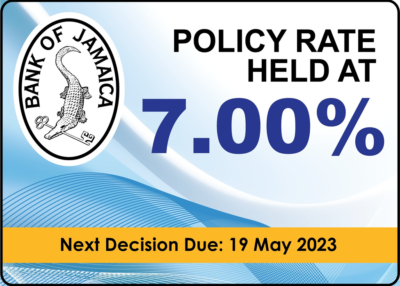

Interest rates held at 7% for Jamaica

Interest rates set by the Bank of Jamaica held at 7 percent for the overnight deposits, even as inflation continues to fall rapidly in the country and now running at an average of 0.20 percent per month or 2.4 percent annualised since November last year. The monetary Policy Committee determined the decision at meetings held this week.

According to the country’s central bank, “Inflation continued to ease, consistent with Bank of Jamaica’s monetary policy and international developments. Jamaica’s inflation rate to February 2023 of 7.8 percent was below the rate of 8.1 percent at January 2023. The February outturn was the lowest rate since December 2021.”

According to the country’s central bank, “Inflation continued to ease, consistent with Bank of Jamaica’s monetary policy and international developments. Jamaica’s inflation rate to February 2023 of 7.8 percent was below the rate of 8.1 percent at January 2023. The February outturn was the lowest rate since December 2021.”

The key external drivers of headline inflation, such as grains, fuel and shipping prices, continued to decline, broadly in line with the Bank’s expectations. In addition, inflation expectations continued to track.

Core inflation (excluding food and fuel prices from the Consumer Price Index) at February 2023 also decelerated to 6.6 percent from 7.1 percent at January 2023 and is projected to fall further as monetary policy remains tight.

Annual inflation is projected to continue to fall to the Bank’s inflation target range of 4 to 6 percent by the December 2023 quarter. One-off regulated price adjustments may, however, result in a temporary uptick in inflation.

Notwithstanding positive developments in inflation, “the MPC noted that the risks to the inflation outlook remain elevated. In a context where the domestic economy continues to grow, labour market shortages carry the potential for future wage adjustments that can put upward pressure on inflation.

BOJ holds overnight rate.

Higher inflation could also result from a worsening in supply chain conditions and higher commodity prices if there are further geo-political disruptions. Among the factors that could lead to lower-than-projected inflation, weaker-than-expected global growth could negatively affect domestic demand, and some projected adjustments to regulated prices may not materialise.”

“Therefore, to continue underpinning inflation returning to the target range and to underwrite continued stability in the foreign exchange market, the MPC unanimously agreed to hold the policy interest rate at 7 percent, to maintain tight Jamaican dollar liquidity in the money market and to continue fostering relative stability in the foreign exchange market. The Bank’s liquidity management strategy incorporates the impact of the one percentage point increase in the domestic and the foreign currency Cash Reserve Requirements applicable to DTIs, effective the beginning of April 2023.”

Sharp16% plunge in BOJ CD rate

The latest Bank of Jamaica 30 days CD offer on March 22 resulted in the first significant shift in interest rates, with the average rate plunging by 16 percent to 8.85 percent compared with the previous one held on March 17 2023, delivered an average rate of 10.54 percent.

The drop in rates and the amount of funds in BOJ CDs are the first signals that interest rates will be going down in the months ahead with the low level of inflation the country is now experiencing, with a monthly average of 0.20 percent monthly since November last year accompanied by revaluation of the local currency in recent weeks.

While the previous offer attracted 250 bids amounting to $14.98 billion with yields as high as 13.17 percent, the latest offer pulled in 348 bids valued at $57.86 billion, but only $18 billion was offered.

The highest successful bids for the March 22 offer received 9 percent, down sharply from the March 17 yield. BOJ cut the amount of funds held in CDs to $81.85 billion, down from $92.85 billion for the March 17 offer and $104.5 billion at the February 24 auction, which resulted in an average interest rate of 9.87 percent. BOJ has eased the tight liquidity that characterized the market for several weeks.

Remittances up in January for Jamaica

Remittance inflows into Jamaica rose 2 percent to US$248.6 million for January 2023, up from US$243.7 in 2022, data out of Jamaica’s central bank show and represent the 6th monthly increase since January last year, with increases in the first two months of the year, as well as August, November and December.

The slow increase for January is in stark contrast to some others in the region. Guatemala and Mexico with growth of 17.4 percent and 12.5 percent respectively and El Salvador with an increase of 6.4 percent, the Bank of Jamaica report shows.

The slow increase for January is in stark contrast to some others in the region. Guatemala and Mexico with growth of 17.4 percent and 12.5 percent respectively and El Salvador with an increase of 6.4 percent, the Bank of Jamaica report shows.

Remittances in 2021 amounted to 58 percent of Imports, down from 61 percent in 2020 but only 37 percent in 2019 and 135 percent of the inflows from the tourist industry in 2021, 206 percent in 2020 and 67 percent in 2019. The ratio for tourism would have declined in 2022 and below the 100 percent level for 2023 based on the sharp recovery in that industry in 2022 and so far in 2023.

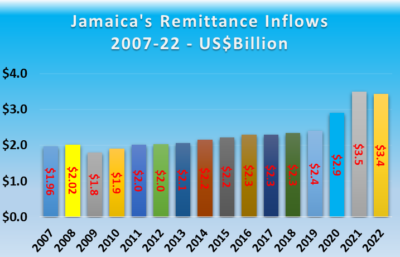

Remittance inflows to Jamaica fall

Remittances inflows to Jamaica amounted to US$3.440 billion in 2022 a 1.6 percent fall from inflows of US$3.497 billion in 2021, the first year of decline since 2014, data out of Bank of Jamaica show.

2022 is the second year that inflows exceeded the $3 billion mark, although 2021 came close with $2.905, $492 million in excess of inflows for 2020.

Inflows for December last year were slightly ahead of 2021, with inflows of US$326 coming in the 2022 last month versus US$321.6 for December 2021.

13 Junior Market stocks to watch in 2023

To make the 2023 ICTOP15, projected gains have to exceed 280 percent over the next 18 months at a projected PE of 22.5 times earnings. That level of growth is what the lowest on the list, Access Financial is projected to deliver over the period.

To make the 2023 ICTOP15, projected gains have to exceed 280 percent over the next 18 months at a projected PE of 22.5 times earnings. That level of growth is what the lowest on the list, Access Financial is projected to deliver over the period.

So great are the prospects of the Junior Market that IC Insider.com thought it important to highlight these additional companies for investors to see the great potential to make money over the next 18 months. This publication has never before put out such a list to start the year, in addition to the ICTOP15.

While the IC TOP15 2023 listings reflect 15 companies that show the greatest potential to be the top performers up to May 2024, a number of companies have the potential to do exceedingly well over the period but are likely to underperform those in the ICTOP15, even then, the future is not assured and some in the watch list could outperform projections and end in the top performers for the period.

The watch list shows that investors do not have to hit home runs to make decent gains in the stock market, but observation in the local market suggests that many persons may not have the patience to build gains over time.

These may or may not be the best companies in the market based on management, products or services and financial health, but they are undervalued and could deliver above average gains as well as pay attractive dividends in the 2023 to 2024 period.

These may or may not be the best companies in the market based on management, products or services and financial health, but they are undervalued and could deliver above average gains as well as pay attractive dividends in the 2023 to 2024 period.

The market has demonstrated that the ability to increase profits is the most important factor that will drive stock prices and is the primary area for investors to focus on going forward.

CAC2000 Projection EPS $1.

The company has the potential to do exceedingly well, especially with an upsurge in the construction of homes and hotels. But it is not without risk and disappointment from quarter to quarter as projects take time to complete, resulting in jerkiness in earnings. This is definitely a stock to consider from a longer time horizon and not one that can be relied on to deliver instant gains, but it could surprise.

Cargo Handlers

This company is not one that will be on every investor’s list for 2023, don’t let that dissuade you from taking a closer look. One of the smaller Junior Market companies and is highly profitable and holds over $500 million in cash funds and with add to it yearly. The company serves one of the fastest growing regions of Jamaica with the continued expansion of the tourist sector that fuels above average economic activities and the BPO sector that lead to increased imports through the Montego Bay port where its operation is centred. Last year’s earnings per share were 77 cents and ICInsider.com is forecasting $1.10 for the current year, that should be enough to push the price towards $20 or more.

An important factor to consider is the cash that they hold which is available for investment in other entities that could add to improved profits going forward. By the way, don’t ignore the dividends they pay.

Dollar Financial came to the Junior Market in June last year and is now accredited by Bank of Jamaica to operate as a micro financial institution. For the nine months to September 2022, profit before tax amounted to $201 million, 257 percent higher than in 2021. Profit before tax for the quarter ending September 2022 increased a solid 214 percent to $70 million, an indication of what could be coming down the road.

Dollar Financial came to the Junior Market in June last year and is now accredited by Bank of Jamaica to operate as a micro financial institution. For the nine months to September 2022, profit before tax amounted to $201 million, 257 percent higher than in 2021. Profit before tax for the quarter ending September 2022 increased a solid 214 percent to $70 million, an indication of what could be coming down the road.

The increase in profits was fueled by loans receivable of $1.2 billion to September 2022, an increase of $650 million or 125 percent over the September 2021 position. Up to September, secured loans represented 72 percent of total loans and unsecured 28 percent.

The company recently raised $1.17 billion in debt financing and expanded the resources available for lending. These funds plus additional cash from profit to be generated provide more than adequate fuel for strong loan expansion that will result in continued above average profit growth. The company plans to use some of the funds raised to expand to the Bahamas and the Eastern Caribbean and capitalize Ultra Financier Limited, their asset based lender. The company could turn out to be exceptionally profitable if the resources are managed well to prevent heavy loan loss provisioning that could eat away at profits. ICInsider.com projects earnings of 35 cents per share for 2023 and that should be good enough to send the stock flying with gains of more than 200 percent.

Express Catering EPS is projected at 65 cents for 2023/4

The company started to benefit from the rebound in tourism but importantly the first half of the 2022 calendar year saw a decline in visitor arrivals compare to 2019, with the numbers for 2023 set to show a major increase over 2022first quarter numbers. The first quarter should be up over 50 plus percent compared with that of 2022. That will have a major impact on the revenues, with its entire operation within the Sangster International Airport. It is worth noting also that the company will have additional restaurants within the airport during the new fiscal year and this is going to add to revenues and profitability for the company.

With the stock price hovering around $5 per share this stock is selling slightly less than eight times earnings and shows the potential to do even better than the revenues and the earnings per share projections. With many Junior Market companies selling at PE ratios around 20 one should expect the stock to deliver a 200 percent rise in value over the next 18 months or so.

Fontana stock could gain 150 percent for the period. looking back, for the first quarter to September, revenues rose a healthy 26 percent and profit jumped 43 percent to $87 million. The projection is for revenues to continue to grow around the 26 percent level into 2023, with profit to rise to 80 cents per share for the year and $1.50 in the 2024 fiscal year ending June. With the stock priced around $9 it is nicely positioned for a bounce to provide an excellent return over the next year and a half.

Fontana stock could gain 150 percent for the period. looking back, for the first quarter to September, revenues rose a healthy 26 percent and profit jumped 43 percent to $87 million. The projection is for revenues to continue to grow around the 26 percent level into 2023, with profit to rise to 80 cents per share for the year and $1.50 in the 2024 fiscal year ending June. With the stock priced around $9 it is nicely positioned for a bounce to provide an excellent return over the next year and a half.

The company is adding a new store in Portmore that should come into operation during the first half of 2023 and add revenues and profits to the business, but this may not be significant until the 2024 fiscal year. Expected growth in the local economy and a big bounce in tourism traffic will have a positive impact on stores in the western end of the country and deliver increased revenues and increased profit as a result. For the year to June 2022, profit was up 12 percent to $415 million from a 21 percent rise in revenues to $4.7 billion.

Image Plus Consultants – EPS 30 cents 2023 and $0.35 for 2023-4

The Image Plus stock failed to sparkle on listing in January, rising just 10 percent by the close of its first day on the market in heavy trading of nearly 12.4 million shares, the second heaviest traded Junior Market stock on opening, following an IPO. The price has now fallen below the issue price providing a good entry point for investors but has since bounced just above $2 with the release of nine months’ results to November. (See articles on analyzing the IPO and the nine months’ results.)

Jamaican Teas – earnings could hit 30 cents per share for the current fiscal year. Some input costs have declined following shipping facilities normalizing, resulting in lower shipping costs as well a reduction in some raw material prices worldwide. The forecast includes a sizable contribution from QWI Investments and a contribution from the real estate development that should see sales of its current development being concluded in the current fiscal year.

The group is expanding the product range for the local and export markets which will add to revenues and profits going forward.

The stock has seen increased buying from individual and institutional investors which is an excellent sign as it lends solid support for trading.

Knutsford Express

Knutsford Express – projected EPS of $1 and $1.40 for 2024.

The company suffered, in a meaningful way, from lower revenues when business activities were severely curtailed with the advent of the Covid-19 pandemic in Jamaica which resulted in major disruption in the economy. In the latest fiscal year to May, revenues were back to pre-pandemic levels in dollar terms but profits lagged as increased costs grew faster than revenues, resulting in the 2022 full year results being 38 percent of 2019 but more than twice 2020.

For the August quarter, revenues rose 78 percent to $415 million and profit jumped from $9 million to $84 million. For the half year to November, revenues rose to $813 million from $473 million in 2021 with profit surging from $13 million after tax to $143 million. Third quarter profit rose from just $2 post-tax to $59 million. The Drax Hall Business Centre is contributing fully to profit with all available space occupied with several tenants already open for business and the company looking to generate income in the order of $100 million a year from the complex.

The company is benefiting from the upsurge in visitor arrivals both directly and indirectly from persons working in the industry.

Main Event returns to IC TOP 10.

Main Event – EPS is projected at $1.10 for 2023

There is the potential for the stock price to gain 180 percent over the next 18 months. Profits for the nine months last year jumped 147 percent to $243 million over 2021 as revenues rose from $501 million to just over $1 billion dollars representing 85 percent increase over the previous year. Revenues for the September quarter rose 147 percent to $602 million with profits for the quarter jumping a solid 332 percent to $104 million as profits rose by $95 million over the previous year, suggesting that the results of 2022 will be outstanding and that could carry over well into 2023.

What is worth noting is that revenues for the first quarter were just $203 million and for the April quarter $290 million, well below third quarter numbers. By contrast, revenues were $458 million in the first quarter of 2019 and $438 million in the second quarter, well ahead of those for the 2022 periods, this has a lot of significance for revenue growth in the first half of the 2023 year. The data show that there should be a significant pick up in revenues and profitability in the corresponding 2023 period and a major uptick in revenues for the year and profits. There is a bit of seasonality in earnings and this could have implications in 2023. The final results for 2022 will provide good guidance on this.

The lesson to be drawn from the numbers for the first three quarters of the year is that profit for 2023 will be up substantially up on the ultimate results for 2022. There is a level of uncertainty along with various developments in the local economy that makes it challenging to project with certainty the level of business that Main Event will undertake, this is the major reason why the stock is placed on the watch list. The final numbers could impact the stock price significantly.

Of note, the third quarter revenues are the highest record in the company’s history in the quarter. The company indicates that the increased business was due to added activity in its core business. The entertainment industry has seen a strong return to outdoor events and lifestyle experiences after a two year break.

Medical Disposables EPS is projected at 40 cents for fiscal 2023 and 70 cents for 2024

This company is not one to take at face value as they quietly build the infrastructure on which to deliver increased business going forward. The company is focusing on laying the foundation for growth in consumer products as increased business opportunities in the medical area slow. The dental area that is operated by the newly formed subsidiary has room for expansion outside of the western region and should be able to ride on the parent company’s infrastructure that currently exists in the next year or two.

The company in the meantime has increased expenditure to attract and keep talent within its employ to grow business, this development resulted in increased costs in the current fiscal year and negatively affected growth in profits for the fiscal year to date.

There is the possibility that more shares could be available in the market over the next year or so.

One on One Educational EPS is projected at 20 cents

The stock raced out the blocks on the fifth day of listing in the latter part of last year to hit $2.50 but the price has fallen to a low of $1.10 in December, with investors concerned that they may have lost a major client and the negative impact that may have on profit. The prospectus stated that in August 2021, 63 percent of the Company’s revenue came through Business to Business contracts and 37 percent through the Company’s end user consumers’ business line. Neither the 2022 audited accounts nor the first quarter results show any fall out of business, in fact, revenues almost doubled in the quarter with profit rising to $12 million before tax from a loss of $1.8 million in 2021. The price could be considered appropriate based on results released so far but as more results become available, the current price may appear to be a gift.

Funds raised in the public issue in 2022 net of loan repayment were earmarked for the development of technological infrastructure for expansion. Regardless, the major reasons to invest in this company is not its short-term fortunes or misfortunes but the major potential its operations have to deliver above average growth within Jamaica and overseas.

Spur Tree Spices EPS is projected at 40 cents.

Spur Tree Spices EPS is projected at 40 cents.

The company recorded a 9.4 percent growth in revenues to $672M for the nine-months ended September 2022, from $614 million in 2021. Gross Margin increased from 31 percent in 2021 to 35.4 percent in 2022.

For the September quarter revenues slipped to $233 million from $247 but improved profit margin resulted in a gross profit of $75 million versus $73 million in the prior year. Profit before Taxation fell to $30 million in the quarter from $33 million in 2021, but climbed 30 percent to $119 million for the year to September compared with $91 million in 2021 and was just shy of the $124 million for the full year in 2021.

The company implemented investment projects to expand the Exotic Products factory infrastructure to double production capacity, purchase of building in Port Morant to establish a production facility and upgraded the Spur Tree Spices production capacity.

They also advanced $100 million to purchase a controlling interest in Canco, an ackee canning company, and if combined with Exotic Products could result in a major jump in production and improved efficiency. They also appointed Massy Distributions agents for regional distribution.

This company has a lot of promise but the valuation placed on the stock ran ahead of results as such improved results in 2023 are unlikely to be reflected fully in the stock price and provide above average growth for the stock but it could be good enough to deliver a reasonable gain that investors would be normally pleased with even if it does not put it in the top ranking of stocks. Additionally, it has growth potential going beyond 2023 that could help deliver above average long term growth.

Stationery & Office Supplies recording record 2022 profits.

Stationary and Office Supplies should deliver gains of 250 percent for the period. The company has done exceptionally well in 2022 and is one of the top performing stocks for that year, gaining 140 percent as a result of very strong profit performance during the year that came from an incredible 60 percent increase in revenues that should end close to $1.8 billion for the year and $2.3 billion for 2023. The company generated a profit of $250 million for the nine months to September that should reach $360 million for the full year and just over $550 million in 2023.

ICInsider.com does not expect the performance to be at the same level in 2023 but sees continued attractive growth in earnings that should put it at about $2.20 per share, up from around $1.35 per share in 2022.

The business continues to increase from local and overseas demand. Information is that a deal was struck with a Trinidad company to sell their furniture in that market in addition the possibility exists that they could be getting into other Caribbean countries to add to the organic growth of the business. There is the possibility for acquisitions of small businesses during the year that could benefit from synergies within the company and deliver above average returns from such investments. Investors should not ignore the possibility of a stock split that could provide additional spice to make the performance of the stock an attractive one.

Finally, the company is well managed and financially healthy with limited debt and increasing shareholders’ equity.

Jamaica’s economy looking great for 2023

The Jamaican economy could grow by more than 6 percent in 2022, with continued growth in tourism and the Alcoa Alumina plant back in production in late August and could lift the December quarter growth above the 5.9 percent that Statin reported for the September quarter. The strong second half year growth should carry over into 2023, coming from an average increase of 5.73 percent for the period up to September and will be boosted by the expected continued strong resurgence of the tourism sector in 2023, barring unforeseen adverse developments, along with the impact of production from the reopening of the Jamalco Alumina plant that will add quite a bit to growth going into the first half of 2023.

Mining to contribute to GDP gains in 2023

Inflation is still not entirely under control yet, but it peaked in 2021, with the average for 2022 running close to the upper end of the central bank’s target of 4 to 6 percent. Developments that should help decrease the rate include world oil prices that have fallen substantially from the over $US120 experienced after the Ukraine war started and are now around US$80 a barrel. Prices of some other commodities are reduced and others could follow as a push of interest rates by several developed countries is set to tighten economic activities and trim demand. A tighter labour market, locally, could put upward pressure on wages and prices, but the tighter monetary policy from last year could hold prices down for a while.

Growth is not only expected from the above two areas. Assuming fair weather conditions, Agriculture, the star performer in the economy for several years, should continue its contribution in 2023. The sector will be helped by growth in tourism that feeds off the industry. The BPO sector seems poised to continue to add to growth as well as the construction sector, with continued growth in housing, road construction and the need for factories and warehousing space. There may well be a lull in the sector with the two south coast roads coming to completion in 2023: the Harbour View to Portland leg and the May Pen to Williamsfield leg of Highway 2000. The Montego Bay perimeter road should take over but may not fill the gap. This may not happen until the Montego Bay to Ocho Rios dualisation commences and is well on the way.

Why is tourism so important? Data shows that for the first quarter in 2022, stopover arrivals were 28 percent below arrivals for 2019, with the June quarter off by 3.3 percent, but September to November increased an average of 12 percent, which means that the first quarter in 2023 could see a 50 percent increase over 2019 and much more over 2022 in the first half on 2022.

Tourist arrivals into Jamaica are now running at record levels since August 2022. Data shows the country enjoying four consecutive months of arrivals exceeding similar months in 2019, the previous best period. Airport passenger movements through the Sangster Airport are up an average of 12 percent for the September to November period.

Growth in tourism is expected to be big in 2023

If the recent trend continues, it would mean that stopover arrivals should be in the order of 3 million next year, up from 2,680,920 in 2019 and would exceed those in 2022 by a solid 20 percent, with the winter months enjoying much higher levels of growth as shown above.

The strong rebound in tourism traffic in the first half of the year, compared with 2022, will contribute to above average GDP growth in the first half but will also result in a significant jump in revenues and profits for some companies and the government. This will have significant implications for the foreign exchange market with significantly increased flows, especially in the year’s first half. This development could also impact interest rates as BOJ may no longer have to lend much support to the local currency using high interest rates.

ICinsider.com don’t see interest moving higher and most likely will start to decline before midyear, with inflation within reach of the BOJ target of 4-6 percent in 2022 and with interest rates seeming to peak at 8.46 percent from April 2022 and remaining at the 8 percent level since based on 182 days Treasury bills.

Jamaica’s labour market has tightened and could pressure inflation in 2023.

Unemployment at 6.6 percent in July is expected to fall in 2023 towards the 5 percent region as more workers will be needed to man the economic expansion. This could mean wage increases could rise above normal to retain or attract new workers.

But all the above is good news for the private sector overall, that should see increasing demand for goods and services.

The banking sector showed loans growing at an annual pace of 12 percent up to September 2022, data from the Bank of Jamaica shows up to $1,096 billion, but increased loan rates may be negatively affecting some areas. With what could be a year of reducing interest rates engineered by BOJ, there could be even faster loan growth in 2023 than in 2022.

Remittances in 2022 appear they will fall short of the US$3.5 billion generated in 2021 and could come in at just over $3.4 billion for the year, reaching $2.84 billion to October. It may again slip marginally in 2023 since the big surge that took it from $2.4 billion in 2019 to the $3.5 billion level.

Net International Reserves. Jamaica’s Net International Reserves are in a healthy position with a jump of $75 million to $3.85 billion in November, data released by the Bank of Jamaica shows, an improvement over October at $3.77 billion. This year’s November balance is at the highest monthly balance for 2022 but is down US$150 million from the end of December last year with a net of $4 billion. Data from the Bank of Jamaica shows a US$100 million growth to Mid December 2022 that would push the net to around US$3.95, just shy of US$4 billion. Daily trades in the forex market after mid-December suggest a continued buildup of the reserves that should push it over the US$4 billion mark by the end of 2022, with the exchange rate for the Jamaica dollar appreciating 152 to the US dollar at the end of the year.

Road construction could slow growth in the sector in 2023

With the significant rebound in tourism, a resurgence in the Alumina sector and relatively stable remittances and BPO sectors, the country should enjoy record foreign exchange inflows in 2023.

Developments on the foreign exchange front could result in greater stability in the exchange rate for the local dollar. Investors should not be too surprised if there is some revaluation, especially in the first half.

The entertainment and transportation sectors seem poised to get a shot in the arm and benefit from the rebound in tourism, increased employment in the country and the general buoyancy in the wider economy.

The present government will be in power for three years at the end of August, but the last public opinion polls indicate a huge lead over the opposition party; with such a lead, the government is in the driver’s seat as to when elections will be called. But the opposition party could start revving up their machinery, so there could be a fair bit of noise to contend with. Local government elections are due in 2023 and barring some significant negative development these elections appear as if they will proceed as planned. If the opposition does well in these elections, it could result in the political heat being turned up a notch or two. If they don’t things will quiet down as the odds favour the government going the full term.

The above are positive developments but investors cannot ignore the impact that the war in Ukraine has had and could have going forward as well as concerns about the covid19 problems in China and how that could affect the world economies.

Reports to follow – Interest rates and the stock market. Outlook for stocks in 2023. Top 15 stocks. Stocks to watch in 2023.