Image courtesy of suphakit73/FreeDigitalPhotos.net

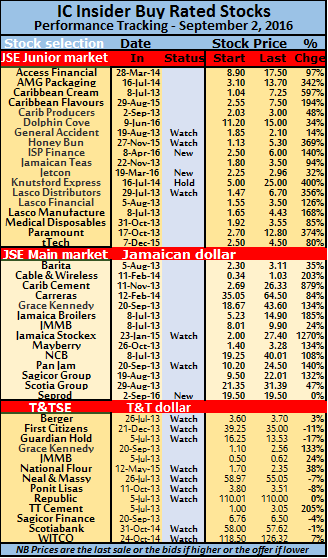

The Jamaican market has seen strong reaction by investors on the announcement of stock splits with the price of each company stock climbing. IC Insider added Seprod to the list while lifting the watch on Sagicor Group, thus restoring a BUY RATED status on it. There are no other changes to the list.

AMG Packaging is IC Insider’s top junior market stock for growth in the next 12 months.

Caribbean Flavours price lost flight earlier this year, but with reported audited earnings of $0.82 per share, the price is rebounding. Caribbean Producers suffered from competitive pressures in the Jamaican market and wrote down inventory but should see some reversal of that pressure in the New Year.

However, it does not have a high ranking on the BUY RATED list at this time. Dolphin Cove is up 34 percent since its recent elevation to the BUY RATED list and should trend higher. ISP Finance, a recent addition, gained 140 percent since listing. The company is in the process of raising funds through a bond issue, which will provide funding for an expanded loan portfolio. The stock is very scarce, but 2017 could be a big year for the company and the stock.

Investors are ignoring the robust profit performance of Jetcon Corporation but may regret it as the price is likely to grow strongly. Profits have climbed nearly 100 percent over 2015 to June,

Barita is the top IC Insider’s stock for growth over the next 12 months in the main market.

In the main Jamaica stock market, Caribbean Cement remains undervalued and is poised for a big price rise as the company increases revenues from a growing economy and reduce cost. Many investors keep focusing only on the reported earnings, but these include one off cost that should be taken out in assessing earnings and value.

Better yet, come 2017 the one off costs won’t be there, importantly, not only will the cost relating to staff separation not be there but the ongoing cost for staffing will be reduced by amounts that approximate redundancy cost. GraceKennedy is benefiting from an improving economy locally and overseas and should see more gains ahead in profits and the stock price.

Better yet, come 2017 the one off costs won’t be there, importantly, not only will the cost relating to staff separation not be there but the ongoing cost for staffing will be reduced by amounts that approximate redundancy cost. GraceKennedy is benefiting from an improving economy locally and overseas and should see more gains ahead in profits and the stock price.IC Insider sees JMMB Group as highly undervalued with decent profit results for the current fiscal year and could surprise to the upside. Barita Investments is having a better 2016 than 2015 and has a big pool of unrealised investment gains on its balance sheet that can be released to profit at any time. The stock seems poised for more growth in the years ahead. Jamaica Stock Exchange’s stock could trend higher with the expectation of a stock split, the price may be getting a bit rich for much short term gains.

IC Insider considers the future to be bright for the stock, as trading activities rise in future years, consequent on growth in the local economy and further declines in interest rates that are bound to drive more money into the market seeking decent return. National Commercial Bank is on target to earn around $6 per share in 2016 while Scotia Group’s results to July showed strong growth in the second quarter over 2015, suggesting that increased profits are once more on the table for this entity. Investors should consider that the year end for these two entities is September and October as such very early in 2017 fresh results will be out before even some of companies with 2016 December year end, release their final numbers for this year. Seprod is engaged in cutting cost in various areas and with growth in the economy, the company is in a good position to do well for investors.

The Trinidad market remains a tough one with the price of oil under pressure. Trinidad Cement seems the only compelling buy, but pressure in the construction sector will be seen as negative for the company.