Access Financial Services profit has grown regularly from 2005 to 2017.

“I recently began trading stocks on both the main and junior market, and I was hoping that you could guide me through the analysis of the market and stocks and IPOs, I am not sure which stocks might likely break out on either market and my portfolio is sitting in the red for a year now,” a reader asked recently.

That is a bit tough when several stocks have delivered very good returns in 2017 with the JSE main market up more than 50 percent for the year to date and with 9 Junior Market stocks rising more than 100 percent. It is worth noting that investment is not an endeavor that will always produce quick positive results. One of the stocks in the portfolio was clearly bought at far too high a price and value. Currently, although the price has fallen it can be considered overpriced. If you were following IC Insider.com you would have seen from last year that the stock was highly overvalued. Important it was the top performing Junior Market stock and there is good evidence suggesting that buying the top performing stock for a year is unlikely see that stock performing strongly in a subsequent year.

JMMB peaked in 2005 and only exceeded that price in 2017.

The number one rule in investing, get good reliable advice. Rule number 2, compare the price earnings ratios of stocks and focus on those that are the lowest and those companies that are doing well, that is, their profits are growing in a consistent manner and likely to continue that way into the future. A very good case in is that of Access Financial with a virtual increase in profit every year since listing.

Be very careful of popular stocks there may have run their course of gains and have little fuel let to go much higher.

Future earnings are important in investing, but it makes no sense to buy a stock at a high price with the hope that in a few years, profits will then grow and make a profitable investment for an investor, while one waits on the big pay day, other stocks are rising and the investor misses out on other good opportunities. Companies that are expanding can provide good investment opportunities.

Three stocks in the Jamaican market, made historical highs in 2005 and it was not been until 2017, that two recovered enough to exceed the previous highs, these two are JMMB Group and Scotia Group. Mayberry Investments is the third and is well below the peak after so many years. Even as two have exceeded the 2005 highs, the gains from then to now, is not very great while many others have gone on to record considerable gains. The lesson from these three is that, while investors wait to recover losses by holding on to poorly performing assets, they are missing profitable investment opportunities elsewhere.

Stock market moves in opposite direction to interest rates.

Why is it so important to get good advice? In August a brokerage house recommended that investors sell Caribbean Cement as in their opinion it was overvalued. At the same time IC Insider.com had the stock highly placed in the TOP 10 stocks to buy. The other is Berger Paints where some investors sold their stock for $10.88 only to see a big price gains since. Some persons have not factored in a number of developments in some of these companies and other developments in the wider economies, all of which can push revenues and profits. What are some of these, Cement has cut cost and likely to do so in 2018 when they refinance the current leasing arrangement. Most importantly, demand for cement is going to explode locally as demand for construction rise. The same will be happening at Berger as more buildings mean more demand for paints.

Consistent growth| Most investors should really be investing in companies where there is a consistency in annual growth in profits. They should shun ones with a checkered earnings history, unless they can be adept of picking tops and bottoms. That is a task persons who use technical analysis can do well.

Dangers of investing| When stock prices rise much faster than the growth in profits, it is time to take serious note of what is happening, this is a telltale sign of a correction ahead, unless the company is recovering from past period of undervaluation, interest rates are falling or the company is expanding and will be expected to enjoy a boost in profit as a result. Investors in such stocks should be fully conversant with what are the factors at play, to ensure their investment can be properly protected if, and when, the factors change.

Other factors| Look at developments in each company and what is happening to the local economy and the likely impact on companies. Most importantly, movement in interest rates have been shown to move markets in one direction or the other and this is a critical factor in investment assessment. One last point to bear in mind is the Investor’s Choice 80/20 rule.

The 80/20 rule| The rule is simple but profound, only 20 percent of the stocks that end up in the top 10 in one year reenter in the subsequent year and in some years just one or none make it, while 40 percent of the 10 worst performing stocks, make it to the top 10 best performers in the subsequent year. This is backed up by data going back for several years to the 1980s. This rule is only broken in a few years that are bearish. this rule is a very good guide for investors in knowing which stocks to buy or sell and when.

Investors should refrain from the fad of following the leader blindly. In 2013 ICInsider.com posted a report on the

Investors should refrain from the fad of following the leader blindly. In 2013 ICInsider.com posted a report on the

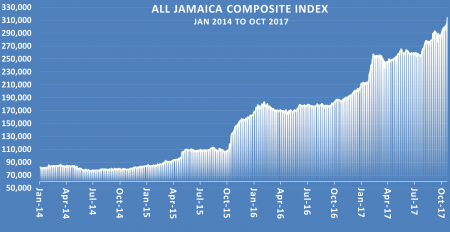

Markets have a way of telling stories that confound many. In May 2014of that year, the local market declined to reach 76,344.27 points on June 23, after reaching 86,590 points in mid-March.

Markets have a way of telling stories that confound many. In May 2014of that year, the local market declined to reach 76,344.27 points on June 23, after reaching 86,590 points in mid-March.

The question of the week comes from one of IC Insider.com’s readers. “ I’m trying to understand more about investing and would like to know about buying stocks at the IPO price, selling when they go up and then buying when the prices settles lower? Does it make sense to do so?

The question of the week comes from one of IC Insider.com’s readers. “ I’m trying to understand more about investing and would like to know about buying stocks at the IPO price, selling when they go up and then buying when the prices settles lower? Does it make sense to do so?

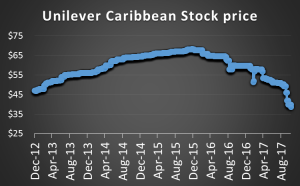

Well it was not until late 2016 that the price exceeded the 2005 high.

Well it was not until late 2016 that the price exceeded the 2005 high.

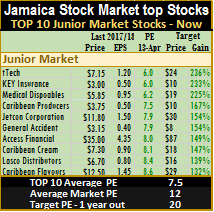

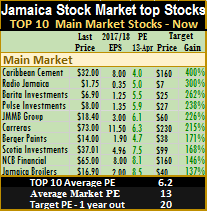

The average PE ratio of both markets are currently at an average of 12, based on this year’s estimated. At the close of the markets on Thursday, IC Insider.com’s TOP 10 Junior Market stocks continue to trade at an average discount of just under 40 percent to the Junior Market average, those in the main market are trading just below 50 percent discount, leaving several stocks with good room for growth for the rest of the year.

The average PE ratio of both markets are currently at an average of 12, based on this year’s estimated. At the close of the markets on Thursday, IC Insider.com’s TOP 10 Junior Market stocks continue to trade at an average discount of just under 40 percent to the Junior Market average, those in the main market are trading just below 50 percent discount, leaving several stocks with good room for growth for the rest of the year. Caribbean Cement continues to trade with a heavy downside bias notwithstanding the rise in price for the week to $32, with last year’s first quarter results dated April 20, this year’s results could be out in the coming week and provide direction for the stock.

Caribbean Cement continues to trade with a heavy downside bias notwithstanding the rise in price for the week to $32, with last year’s first quarter results dated April 20, this year’s results could be out in the coming week and provide direction for the stock.  The payment of dividends is only one element to consider in investing in stocks. Investing companies that do not pay dividends should not matter seriously, in the short.

The payment of dividends is only one element to consider in investing in stocks. Investing companies that do not pay dividends should not matter seriously, in the short.

Do you really know your adviser?

Berger Paints is worth more than $20 per share.

The directors of Berger Paints should have their resignation letters ready for signing after in early October, as their continuing service will be in conflict with the recommendation they gave minority shareholders who seem set to rebuff it.

One of the critics wrote, “I looked over their prospectus the very day it was released and came to the very same conclusion that this price is pie in the sky!! I have a degree in Finance and I invest in companies on the JSE, including Mayberry and I think this is a sad day in IPO valuation. They had the opportunity to set the standard for the Jr. JSE and they are muggin it up. The conclusion I draw from their pricing is that they take the Jamaican investor for idiots, like so many companies in Jamaica. And they are playing on peoples’ greed. I would love to invest in this company and if it hits the market I will wait for the price to realign to it’s proper valuation before buying.”

One of the critics wrote, “I looked over their prospectus the very day it was released and came to the very same conclusion that this price is pie in the sky!! I have a degree in Finance and I invest in companies on the JSE, including Mayberry and I think this is a sad day in IPO valuation. They had the opportunity to set the standard for the Jr. JSE and they are muggin it up. The conclusion I draw from their pricing is that they take the Jamaican investor for idiots, like so many companies in Jamaica. And they are playing on peoples’ greed. I would love to invest in this company and if it hits the market I will wait for the price to realign to it’s proper valuation before buying.”

In response to my article saying the market is huge the reader had this to say,“How is the market huge when this company’s business model caters to small and micro business sector? Take an informal survey on how many micro business have pulled down their shutter since the year started. If I did not have access to information I might have called you for guidance as a stockbroker, what a disappointment that would have been.”

In response to my article saying the market is huge the reader had this to say,“How is the market huge when this company’s business model caters to small and micro business sector? Take an informal survey on how many micro business have pulled down their shutter since the year started. If I did not have access to information I might have called you for guidance as a stockbroker, what a disappointment that would have been.”

Investors need to be adequately informed as there are wolves out there to help snatch valuables from them. Salada Foods is a very profitable entity after the broker to a takeover offer and audit firm recommended shareholders to sell their shares for an undervalued amount back in the 1980s. According to the auditor, the plant was obsolete and coffee powder was no longer accepted by consumers. The broker suggested that minority shareholders will have to eat their shares for their stupidity in not accepting the offer. Three decades on and the company remains profitable and debt free and those shareholders who held their shares have done extremely well by doing so. I wrote at the time of the offer that it was unfair. I gathered that the chairman Mr. Charles Ransom at the time, on a flight back to Jamaica, dammed John Jackson for killing the offer, when he saw the story that was highly critical of the offer. That was a few days before the vote that rejected the offer.

In 2010 the first Junior Market listing IPO was condemned outright by a featured article in the Friday Business Observer, followed by a series of comments by doomsayers. The arguments against the offer were so uninformed that I wrote an article defending it fully.

And yet another investors comments, “Mr. Jackson everyone has a right to his or her opinion, you Sir should have done your homework. I am not a stock broker, but I was interested in the offer and did my research, after reading the Prospectus I decided not to take up the offer.”

“Look at likely future earnings, the future of Access Financial looks BAD. WHAT IS THEIR BUSINESS??? SUB-PRIME LOANS. In the USA a company such as this would be called a predatory Lender. The business model looked okay 3 to 4 years ago, but now it just looks dismal. Most of the clients the forward looking statement alludes to are people who live paycheck to paycheck. With all the talk of layoffs and cutback in the Jamaican economy, how does the principal of Access expect their business to grow?”

“One point made in the prospectus is that Government does not regulate this particular company, and therefore they can keep their interest rate on their products higher. Look at the percentage of bad loans recorded for 2008, and then compare that to the 9.09% projected non-performing loans in the prospectus. Come now Mr. Jackson, does this sound right to you?”

My current response, they made a big mistake in reading the prospectus first, as they would have done far better had they done the right thing. One investors who was advised to buy, did just that and enjoyed wonderful returns.

Earlier this year, a brokerage house was recommending Cargo Handlers as a buy in the $20 range when the PE ratio was in the 50 region. Another last year recommended investors sell Barita Investments, saying the stock was not worth much more than just over $2. Where are these two stocks at presently? One is much lower than the recommendation and one much higher? And for naysayers in Access Financial who cause a number of persons to stay out of Access, they may have learnt from the experience, hopefully as the stock now trades at the equivalent of $460 per share and never fell below the issued price once. In addition investors have reaped a large amount in dividends and the growth goes on. The Berger Paints recommendation to sell is just another of those poor valuations done by persons who don’t really know how to value listed companies. The market will speak in a few weeks on this.