The main market of the Jamaica Stock Exchange climbed new shortly after trading opened on Wednesday, with the All Jamaican Composite Index surging over 366,792.29 points level but by after 13 minutes of trading it shot up 6,924.07 points to 372,546.73.

The main market of the Jamaica Stock Exchange climbed new shortly after trading opened on Wednesday, with the All Jamaican Composite Index surging over 366,792.29 points level but by after 13 minutes of trading it shot up 6,924.07 points to 372,546.73.

With less than a minute after opening the All Jamaica Composite Index rose 1,169.63 points to a new record of 365,792.29 within a minute of opening but that was before NCB Financial traded and jumped to a record high of $125. The JSE Index climbed 1,065.66 points to a record 334,189.24 initially and then to a higher high of 339,432.19 having added 6,308.61 after the NCB jump.

The Junior Market added less than a point to 3,267.31 but Derrimon Trading that will trade x split with the approval of a 10 to 1 stock split is yet to trade.

All Jamaica jumps to 372,546 points

Big bounce in Fosrich profit

FosRich profits rose sharply in 2018

Fosrich Group reported profit of $30 million for the June quarter, an increase of 630 percent over the $4 million reported for the prior year’s reporting period.

Profit before tax climbed to $60.6 million for the half year to June, for an increase of 144 percent over the $25 million for the similar period in 2017 and by an increase of 234% over the post-tax profit of $18 million, reported for the prior reporting period.

Having listed on the Jamaica Stock exchange Junior market in 2017, profits are now free form taxes for a period of 5 years. Earnings per stock unit ended at 12 cents for the half year and 6 cents for the quarter and should end up just around 27 to 30 cents, if the trend continues.

During the second quarter, the company enjoyed an 18.7 percent hike in income to $320 million, from $270 million for the prior year. For the half year, sales revenues were just up by 5 percent to $592 million from $565 million in 2017.

Gross profit for the quarter, rose 23 percent to $141 million from $115 million, in the prior reporting period and for the six months to June gross profit increased just 6 percent to $269 million. Gross profit margin slipped from the first quarter to 44 percent with the margin for the six months ending at 45 percent. Other income for the year-to-date benefited from foreign exchange gains of $15 million.

Administrative expenses fell $14 million for the half year, to $198 million and slipped just slightly for the quarter to $102 million from $103 million. According to the Managing Director, Cecil Foster, “the decrease was driven primarily by efficiencies gained from the management of staff and related costs, reductions in selling and marketing expenses, reduced insurance costs and reductions in damaged goods write-off and warranty expenses. The cost savings were partially offset by increases in staff training, legal and professional fees, rent and bank charges,” management indicated.

Finance cost for the year-to-date was $28.5 million compared to $19.6 million for the prior reporting period, but rose 68 percent in the June quarter to $17.5 million. “This increase is being driven by a new working capital line of credit obtained to assist with the financing of operations. This new facility was obtained at more favourable rates than the previous bank facilities,” Foster advised, in his commentary on the interim results.

Finance cost for the year-to-date was $28.5 million compared to $19.6 million for the prior reporting period, but rose 68 percent in the June quarter to $17.5 million. “This increase is being driven by a new working capital line of credit obtained to assist with the financing of operations. This new facility was obtained at more favourable rates than the previous bank facilities,” Foster advised, in his commentary on the interim results.

Inventories rose sharply from $625 million in December to $808 million in June, receivables declined to $148 million from $156 million. Amounts due to creditors fell sharply from $297 million as of December to just $35 million. The company paid off amounts due on overseas line of credit thus reducing foreign exchange risk. The switch contributed to a sharp rise in loans from $384 million to $795 million.

“The company continues to closely manage inventory balances and the supply-chain, with a view to ensuring that inventory balances being carried are optimised, relative to the pace of sales, the time between the orders being made and when goods become available for sale, to avoid both overstocking and stock-outs. Monitoring is both at the individual product level and by product categories,” foster advised shareholders.

Part of the loans was on lent to an affiliated company that is completing an apartment complex on Shortwood Road, the managing director confirmed to IC Insider.com. The financials show $243 million due form them. The amount due incurs interest at 12.5 percent rate, Foster stated. The line allowed the company to stock up on some commodities at low prices relative to what normally obtains in the trade.

Shareholders’ equity now stands at $670 million, up from the $609 million at December 2017. Fosrich trades on the Junior Market at $2.80 on Tuesday, just around 10 times earnings.

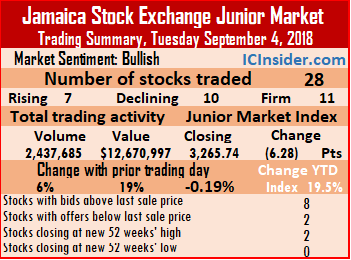

Junior Market slips

Derrimon Trading ended trading at a new closing high of $26.99 on Tuesday.

More prices fell than rose in trading on the Junior Market on Tuesday, with 28 securities being active compared to 26 on Monday, leading to 7 advancing, 10 declining while 11 remained unchanged.

The market closed with the index slipping 6.28 points to close at 3,265.74. Trading resulted in an exchange of 2,437,685 shares valued at $12,670,997 compared to 2,306,821 units valued at $10,660,960, on Monday.

IC bid-offer Indicator|At the end of trading, the Investor’s Choice bid-offer indicator reading had 8 stocks ending with bids higher than their last selling prices, 2 closed with lower offers.

Trading closed with an average of 87,060 units for an average of $452,536 in contrast to 88,724 units for an average of $410,037 on Monday.  Trading for the month to date averages 87,861 shares with an average value of $432,073. Trading in August, averaged 244,613 units at $1,348,298 for each security traded.

Trading for the month to date averages 87,861 shares with an average value of $432,073. Trading in August, averaged 244,613 units at $1,348,298 for each security traded.

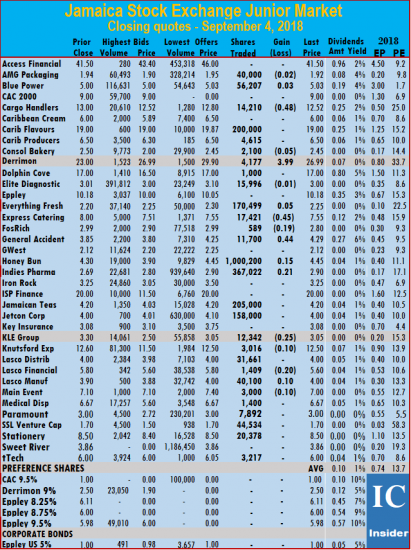

At the close of trading, AMG Packaging ended with a loss of 2 cents at $1.92, trading 40,000 stock units, Blue Power concluded trading of 56,207 units and rose 3 cents to $5.03, Cargo Handlers settled with a loss of 48 cents at $12.52, with 14,210 shares changing hands, Caribbean Flavours traded at $19, in exchanging 200,000 stock units, Caribbean Producers finished trading 4,615 units at $6.50. Consolidated Bakeries closed with a loss of 5 cents at $2.45, with 2,100 shares changing hands, Derrimon Trading jumped $3.99 to end at a 52 weeks’ closing high of $26.99, with 4,177 shares changing hands, Dolphin Cove concluded trading of 1,000 shares at $17, Elite Diagnostic finished with a loss of 1 cent at $3, trading 15,996 stock units. Everything Fresh rose 5 cents in trading 170,499 shares to end at $2.25, Express Catering ended trading 17,421 shares with a loss of 45 cents to close at $7.55, FosRich Group traded with a loss of 19 cents at $2.80, in exchanging 589 shares, General Accident finished trading 11,700 shares and climbed 44 cents to $4.29,  Honey Bun ended 15 cents higher at $4.45, with 1,000,200 units changing hands. Indies Pharma closed at a new high of $2.90, after adding 21 cents and exchanging 367,022 shares, Jamaican Teas settled at $4.20, exchanging 205,000 shares, Jetcon Corporation ended trading 158,000 stock units at $4, KLE Group finished trading with a loss of 25 cents at $3.05, with 12,342 shares, Knutsford Express closed with a loss of 10 cents at $12.50, with 3,016 shares changing hands. Lasco Distributors ended at $4, with 31,661 shares trading, Lasco Financial concluded trading of 1,409 stock units with a loss of 20 cents at $5.60, Lasco Manufacturing finished 10 cents higher at $4, trading 40,100 units, Main Event settled with a loss of 10 cents at $7, with 3,000 shares changing hands. Medical Disposables ended trading at $6.67, with 1,400 shares, Paramount Trading traded 7,892 shares at $3, Stationery and Office finished trading 20,378 stock units at $8.50 and tTech ended at $6, with 3,217 shares changing hands.

Honey Bun ended 15 cents higher at $4.45, with 1,000,200 units changing hands. Indies Pharma closed at a new high of $2.90, after adding 21 cents and exchanging 367,022 shares, Jamaican Teas settled at $4.20, exchanging 205,000 shares, Jetcon Corporation ended trading 158,000 stock units at $4, KLE Group finished trading with a loss of 25 cents at $3.05, with 12,342 shares, Knutsford Express closed with a loss of 10 cents at $12.50, with 3,016 shares changing hands. Lasco Distributors ended at $4, with 31,661 shares trading, Lasco Financial concluded trading of 1,409 stock units with a loss of 20 cents at $5.60, Lasco Manufacturing finished 10 cents higher at $4, trading 40,100 units, Main Event settled with a loss of 10 cents at $7, with 3,000 shares changing hands. Medical Disposables ended trading at $6.67, with 1,400 shares, Paramount Trading traded 7,892 shares at $3, Stationery and Office finished trading 20,378 stock units at $8.50 and tTech ended at $6, with 3,217 shares changing hands.

Prices of securities trading for the day are those at which the last trade took place.

New closing high for JSE main market – Tuesday

The Jamaica Stock Exchange main market continued where it left off on Monday and Friday to scale new heights, as bulls take control of Jamaican stocks, as the market enters the home stretch with less than 4 months left to close the year.

The Jamaica Stock Exchange main market continued where it left off on Monday and Friday to scale new heights, as bulls take control of Jamaican stocks, as the market enters the home stretch with less than 4 months left to close the year.

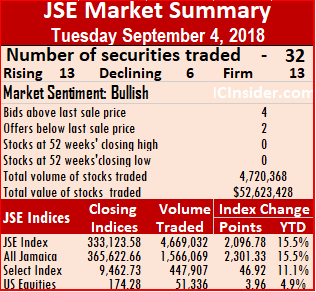

The market closed with the All Jamaican Composite Index jumped 2,301.33 points to end at record close of 365,622.66 and the JSE Index climbed 2,096.78 points to close at record close of 333,123.58. in the morning session the All Jamaican Composite Index jumped to a record high of 366,019.05 points and the JSE Index climbed to 333,484.73 points.

Market activities resulted in 32 securities trading including 2 in the US dollar market compared to 32 securities trading on Monday.  At the end of trading, the prices of 9 stocks rose, 12 declined and 11 closed trading, unchanged.

At the end of trading, the prices of 9 stocks rose, 12 declined and 11 closed trading, unchanged.

Trading in the main market ended with 4,669,032 units valued $51,035,435 compared to 2,406,576 units valued $39,771,123, on Monday.

The day’s volume was led by, Wisynco Group with 1,217,069 shares accounting for 26 percent of the volume traded, followed by JMMB Group 7.50% preference share with 899,400 units and 19.26 percent of the day’s volume and Sygnus Credit Investments with 507,324 units and 10.9 percent of main market volume.

Trading resulted in an average of 155,634 units valued at over $1,701,181, in contrast to 82,985 shares valued at $1,371,418 on Monday. The average volume and value for the month to date amounts to 119,926 units valued at 1,539,094. August closed, with an average of 224,564 shares valued at $4,310,285, for each security traded.

In the main market activity, Caribbean Cement gained 50 cents and finished at $51.50, trading 9,299 shares, Jamaica Broilers traded 57,042 stock units in adding $1 to close at $27, Jamaica Producers finished trading 225,602 units after falling 85 cents to close at $19,![]() Kingston Wharves lost 29 cents and finished at $64, trading 6,927 stock units, PanJam Investment lost $1 and closed at $54, exchanging 6,004 stock units, strong> Sagicor Real Estate Fund rose $1.05 to settle at $12.10, with 8,646 shares trading, Scotia Group rose 50 cents in trading 6,593 units at $53.50 and Seprod finished trading 57,598 shares after falling $2 to end at $43.

Kingston Wharves lost 29 cents and finished at $64, trading 6,927 stock units, PanJam Investment lost $1 and closed at $54, exchanging 6,004 stock units, strong> Sagicor Real Estate Fund rose $1.05 to settle at $12.10, with 8,646 shares trading, Scotia Group rose 50 cents in trading 6,593 units at $53.50 and Seprod finished trading 57,598 shares after falling $2 to end at $43.

Trading in the US dollar market closed with 51,336 units valued US$11,763. Trading ended with Proven Investments exchanging 47,046 shares and rose 1 cent to close at 24 US centsSygnus Credit Investments traded 4,290 shares and lost 0.06 cent to 11 US cents. The JSE USD Equities Index advanced by 3.96 points to close at 174.28.

IC bid-offer Indicator| At the end of trading, the Choice bid-offer indicator reading shows 5 stocks ended with bids higher than their last selling prices and 3 closing with lower offers.

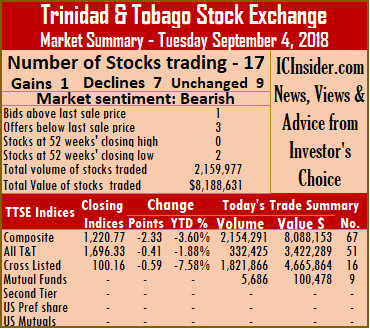

7 stocks fall on TTSE – Tuesday

The Trinidad & Tobago Stock Exchange, declined at the close of trading on Tuesday as declining stocks overwhelmed the one stock to advance.

The Trinidad & Tobago Stock Exchange, declined at the close of trading on Tuesday as declining stocks overwhelmed the one stock to advance.

The market closed with 17 securities changing hands against 15 on Monday, 1 advanced, 7 declined and 9 remained unchanged and trading of 2,159,977 shares at a value of $8,188,631, compared to 168,289 shares valued $2,804,863, previously traded.

At close of the market the, Composite Index the Composite Index lost 2.33 points to 1,220.77, the All T&T Index declined 0.41 points to 1,696.33, while the Cross Listed Index slipped 0.59 points to close at 100.16.

IC bid-offer Indicator| At the end of trading, the Investor’s Choice bid-offer indicator reading closed with 1 stock ending with a higher bid than the last selling price and 3 with lower offers. Two companies closed with prices at 52 weeks’ low.

Stocks closing with gains| Scotiabank concluded trading of 560 shares and rose 66 to end at $65.02.

Stocks closing with gains| When the market closed, First Citizens fell 1 cent to end at $34, after exchanging 2,918 shares, Gaurdian Media closed with a loss of 25 cents and completed trading at a 52 weeks’ low of $15.75, after exchanging 100 shares, Grace Kennedy shed 12 cents and settled at a 52 weeks’ low of $2.70, with 1,550,000 stock units changing hands, Guardian Holdings lost 10 cents and ended at $16.90, trading 5,000 units, JMMB Group ended trading 1 cent lower at $1.70, after exchanging 268,008 shares,  Sagicor Financial concluded trading with a loss of 24 cents and settled at $7.51, with 300 stock units changing hands and Trinidad & Tobago NGL traded with a loss of 9 cents and ended at $29.41, after exchanging 44,065 shares.

Sagicor Financial concluded trading with a loss of 24 cents and settled at $7.51, with 300 stock units changing hands and Trinidad & Tobago NGL traded with a loss of 9 cents and ended at $29.41, after exchanging 44,065 shares.

Stocks trading with no price change| Agostini’s completed trading at $21.11, after exchanging 100 shares, Calypso Macro Index Fund traded 3,290 units to close at $15.80, Clico Investments settled at $20, with 2,396 stock units changing hands, Massy Holdings completed trading at $47, after exchanging 430 shares, National Enterprises settled at $8.95, with 164,535 stock units changing hands, National Flour closed at $1.75, in the exchange of 112,600 units, NCB Financial Group ended at $5.67, after exchanging 3,558 shares, Republic Financial Holdings completed trading at $103.52, after exchanging 1,722 shares and West Indian Tobacco concluded trading of 395 shares at $87.90.

Prices of securities trading for the day are those at which the last trade took place.

All Jamaica breaks 366,000 points

Ending trading at a new record close on the first trading day of September, the Jamaica Stock Exchange climbed new intraday high on the second trading day of the month, with the All Jamaican Composite Index surging over 366,000 points level.

At 12 minutes after opening the All Jamaica Composite Index rose 2,142.96 points to a record 365,464.29 and by 28 minutes after opening it jumped 2,697.72 points to 366,019.05 and the JSE Index climbed 1,952.48 points to a record 332,979.28 and within 2 minutes of 10 o’clock it jumped 2,457.93 to a record 333,484.73

Later on, the market pulled back, with the all Jamaica Index up 1,751.53 to 365,072.86 and the JSE index gaining 1,595.84 to 332,622.64 as NCB Financial pulled back to $112.

The Junior Market lost 17.36 points to 3,255.01.

Major contributor to the early gains, is NCB Financial with a rise to $114.95 from a close of $112 on Monday.

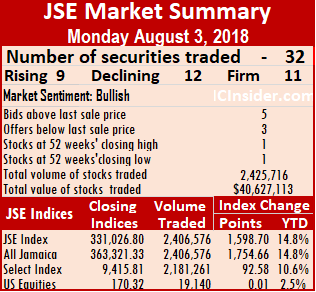

JSE main market surges to new high – Monday

The Jamaica Stock Exchange main market started September off on a bright the market continued from the record breaker run on Friday to end at yet another record close.

The market closed with the All Jamaican Composite Index jumped 1,754.66 points to end at 363,321.33 and the JSE Index climbed 1,598.70 points to 331,026.80.

Market activities resulted in 32 securities trading including 3 in the US dollar market compared to 34 securities trading on Friday. At the end of trading, the prices of 9 stocks rose, 12 declined and 11 closed trading, unchanged.

Trading in the main market ended with 2,406,576 units valued $39,771,123, compared to 8,271,949 units valued at $100,951,929, on Friday.

The day’s volume was led by, Sygnus Credit Investments with 576,849 shares accounting for 23.97 percent of the volume traded, followed by Carreras with 444,645 units 18.48 percent of the day’s volume and Sagicor Real Estate Fund with 440,810 units 18.32 percent of main market volume.

The day’s volume was led by, Sygnus Credit Investments with 576,849 shares accounting for 23.97 percent of the volume traded, followed by Carreras with 444,645 units 18.48 percent of the day’s volume and Sagicor Real Estate Fund with 440,810 units 18.32 percent of main market volume.

Trading resulted in an average of 82,985 units valued at $1,371,418, in contrast to 266,837 shares valued at $3,256,514 on Friday. August closed, with an average of 224,564 shares valued at $4,310,285, for each security traded.

In the main market activity, Berger Paints lost 50 cents and ended at $21, in exchanging 5,775 stock units, Caribbean Cement jumped $1 to finish at $51, with while trading 31,442 shares, Jamaica Producers finished trading 14,365 units and rose $1.35 to end at a 52 weeks’ closing high of $19.85, , Jamaica Broilers ![]() lost 90 cents in trading 10,639 stock units at $26.10, Kingston Wharves climbed $2.49 and finished at $64.29, after trading 8,792 stock units, Sagicor Real Estate Fund lost $1.45 and settled at $11.05, in trading 440,810 shares, Supreme Ventures gained 50 cents and closed at $15.50, exchanging 26,543 shares and Wisynco Group lost 29 cents and concluded trading at $9.20, with 46,051 stock units changing hands.

lost 90 cents in trading 10,639 stock units at $26.10, Kingston Wharves climbed $2.49 and finished at $64.29, after trading 8,792 stock units, Sagicor Real Estate Fund lost $1.45 and settled at $11.05, in trading 440,810 shares, Supreme Ventures gained 50 cents and closed at $15.50, exchanging 26,543 shares and Wisynco Group lost 29 cents and concluded trading at $9.20, with 46,051 stock units changing hands.

Stanley Motta closed at a 52 weeks’ low of $4.40 having lost 17 percent of its value since listing in August.

Trading in the US dollar market closed with 19,140 units valued US$6,248. Trading ended with JMMB group6% preference share ended trading 2,286 shares at 59 US cents, Proven Investments exchanging 16,425 shares to close at 23 US centsSygnus Credit Investments traded 429 shares and lost 0.06 cent to 11 US cents. The JSE USD Equities Index unchanged at 173.74.

IC bid-offer Indicator| At the end of trading, the Choice bid-offer indicator reading shows 5 stocks ended with bids higher than their last selling prices and 3 closing with lower offers.

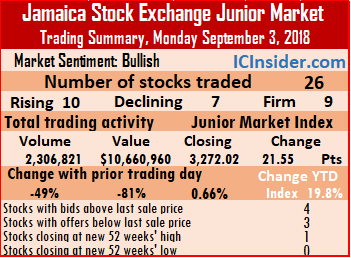

Junior Market opens September positively

Cargo Handlers hits 52 weeks’ high.

Trading slipped on the Junior Market on the first trading day of September, with 26 securities being active down from 30 on Friday as well as a fall in volume and value trading, leading to 10 advancing, 7 declining and 9 remained unchanged.

The market closed with the index rising 21.55 points to close at 3,272.02. A volume of 2,306,821 units valued at $10,660,960 changed hands, compared to 4,503,036 units valued at $56,383,723, on Friday.

IC bid-offer Indicator|At the end of trading, the Investor’s Choice bid-offer indicator reading had 4 stocks ending with bids higher than their last selling prices, 3 closed with lower offers.

Trading closed with an average of 88,724 units for an average of $410,037 in contrast to 150,101 units for an average of $1,879,457 on Friday. Trading in August, averaged 244,613 units at $1,348,298 for each security traded.

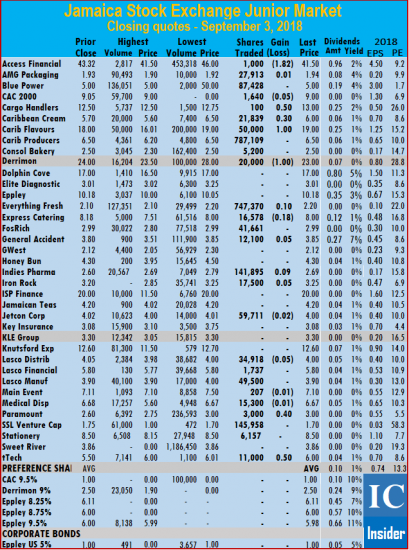

At the close of trading, Access Financial closed with a loss of $1.82 at $41.50, trading 1,000 shares, AMG Packaging ended 1 cent higher at $1.94, with 27,913 stock units changing hands, Blue Power concluded trading at $5, swapping 87,428 units, CAC 2000 finished with a loss of 5 cents at $9, exchanging 1,640 shares, Cargo Handlers settled 50 cents higher to end at a 52 weeks’ high of $13, trading 100 shares. Caribbean Cream ended trading 21,839 shares, 30 cents higher to $6, Caribbean Flavours traded with 50,000 stock units $1 higher to $19, Caribbean Producers finished trading at $6.50, with 787,109 units changing hands, Consolidated Bakeries closed at $2.50, exchanging 5,200 shares.  Derrimon Trading ended with a loss of 1 cent at $23, trading 20,000 shares, Everything Fresh rose 10 cents trading 747,370 shares to end at $2.20, Express Catering ended trading 16,578 shares with a loss of 18 cents to $8, FosRich Group traded at $2.99, with 41,661 shares changing hands, General Accident finished trading 12,100 shares 5 cents higher at $3.85, with. Indies Pharma traded at a new high of $2.80 but pulled back to close at $2.69 after adding 9 cents and exchanging 141,895 shares, Iron Rock concluded trading of 17,500 shares and rose 5 cents to $3.25, Jetcon Corporation ended trading with a loss of 2 cents at $4, in exchanging 59,711 stock units,

Derrimon Trading ended with a loss of 1 cent at $23, trading 20,000 shares, Everything Fresh rose 10 cents trading 747,370 shares to end at $2.20, Express Catering ended trading 16,578 shares with a loss of 18 cents to $8, FosRich Group traded at $2.99, with 41,661 shares changing hands, General Accident finished trading 12,100 shares 5 cents higher at $3.85, with. Indies Pharma traded at a new high of $2.80 but pulled back to close at $2.69 after adding 9 cents and exchanging 141,895 shares, Iron Rock concluded trading of 17,500 shares and rose 5 cents to $3.25, Jetcon Corporation ended trading with a loss of 2 cents at $4, in exchanging 59,711 stock units,  Lasco Distributors ended with a loss of 5 cents at $4, with 34,918 shares changing hands, Lasco Financial concluded trading 1,737 stock units at $5.80. Lasco Manufacturing finished at $3.90, with 49,500 units, Main Event settled with a loss of 1 cent at $7.10, with 207 shares changing hands, Medical Disposables ended trading with a loss of 1 cent at $6.67, with 15,300 shares, after trading earlier at a 52 weeks’ high of $6.70, Paramount Trading climbed 40 cents higher to $3, trading 3,000 shares, Stationery and Office finished trading at $8.50, with 6,157 stock units and tTech ended 50 cents higher at $6, after 11,000 shares changed hands.

Lasco Distributors ended with a loss of 5 cents at $4, with 34,918 shares changing hands, Lasco Financial concluded trading 1,737 stock units at $5.80. Lasco Manufacturing finished at $3.90, with 49,500 units, Main Event settled with a loss of 1 cent at $7.10, with 207 shares changing hands, Medical Disposables ended trading with a loss of 1 cent at $6.67, with 15,300 shares, after trading earlier at a 52 weeks’ high of $6.70, Paramount Trading climbed 40 cents higher to $3, trading 3,000 shares, Stationery and Office finished trading at $8.50, with 6,157 stock units and tTech ended 50 cents higher at $6, after 11,000 shares changed hands.

Prices of securities trading for the day are those at which the last trade took place.

Harris Group buys Antiguan paint business.

Harris Paints Group, the parent company of Jamaican B-H Paints, recently purchased the assets of Lee Wind Paints in Antigua.

Harris Paints Group, the parent company of Jamaican B-H Paints, recently purchased the assets of Lee Wind Paints in Antigua.

The Harris group of companies was established in Barbados in 1972 and is one of the Caribbean’s manufacturers of architectural finishes, building products and industrial coatings.

The group expanded with the acquisition of Brandram-Henderson (B-H Paints) in 2006, a Jamaican paint manufacturer that was founded in 1961.

Harris employs over 200 people across the region, and manufactures paint in Barbados, Dominica, St. Lucia, Guyana and Jamaica. The group distributes paints and related products to over 15 countries in the Caribbean.

Ian Kenyon, CEO-Harris Paints Group, said that the company looked forward to establishing a new manufacturing facility, increasing their investment in the country and that it would provide important strategic access to new export markets such as the BVI, US Virgin Islands, as well as Turks and Caicos.

Over the past six years the Harris Group has seen consistent profitable topline growth across its operations. Kenyon said that these results were achieved despite some very challenging conditions. “The Caribbean has experienced difficult economic times in many of the markets and this has been compounded by the recent severe weather systems across the region, yet our teams in each of the 15 countries we currently sell to, have responded magnificently and have been very successful in achieving profitable market growth and increasing shareholder value. He added, “we are very optimistic about our future as we have built very strong springboards for growth with our investments in infrastructure and have a very exciting portfolio of new product and service innovations ready and primed to launch over the next few years”

This year, the Harris Group also invested and successfully implemented a new state-of-the art enterprise resource planning (ERP) system that integrates all manufacturing plants and functions across the Caribbean, including at the B-H facility in Kingston, providing improved business efficiency and a comprehensive digital platform that will strengthen their marketing capability.