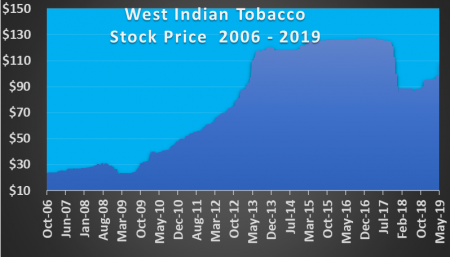

West Indian tobacco closed at a 52 weeks’ high of $112.

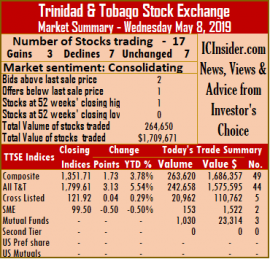

Market activity on the Trinidad & Tobago Stock Exchange ended with big gains in the market indices on Thursday.

Trading took place in 12 securities against 17 on Wednesday, with 5 advancing, 3 declining and 4 remaining unchanged and resulted in the Composite Index climbing 7.67 points to 1,359.38, the All T&T Index jumping 15.07 points to 1,814.68 and the Cross Listed Index adding just 0.01 points to close at 121.93.

Trading ended with 106,666 shares at a value of $2,353,874 changing hands, compared to 264,650 shares at a value of $1,709,671.

IC bid-offer Indicator|The Investor’s Choice bid-offer ended at 3 stocks with bids higher than their last selling prices and none closed with a lower offer.

Stocks ending with gains| At the close of the market, Clico Investments gained 38 cents in close at $23.03, with an exchange of 53,317 stock units,  First Citizens Bank gained $2 to end at 52 weeks’ high of $40, after exchanging just 424 shares. One Caribbean Media added 5 cents and completed trading of 16,000 shares at $10.30, Trinidad & Tobago NGL rose 50 cents in trading 11,555 units to end at $30 and West Indian Tobacco jumped $2 to a 52 weeks’ high of $112, with 940 stock units changing hands.

First Citizens Bank gained $2 to end at 52 weeks’ high of $40, after exchanging just 424 shares. One Caribbean Media added 5 cents and completed trading of 16,000 shares at $10.30, Trinidad & Tobago NGL rose 50 cents in trading 11,555 units to end at $30 and West Indian Tobacco jumped $2 to a 52 weeks’ high of $112, with 940 stock units changing hands.

Stocks closing with losses| Ansa McAl declined 6 cents to $55.30, with 790 stock units changing hands, Massy Holdings fell 20 cents trading of 5,750 at $54.80 and Sagicor Financial closed with a rise of 1 cent at $8.75 in trading of 500 shares,

Stocks closing firm| First Caribbean International Bank closed trading of 3,000 units at $8.35, Prestige Holdings closed at $9, with 389 units changing hands, Trinidad Cement ended at $2.75, after exchanging 11,244 shares and Unilever Caribbean closed at $26.30, after exchanging 2,747 shares.

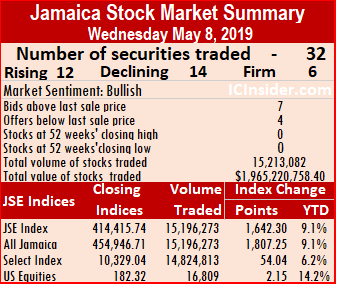

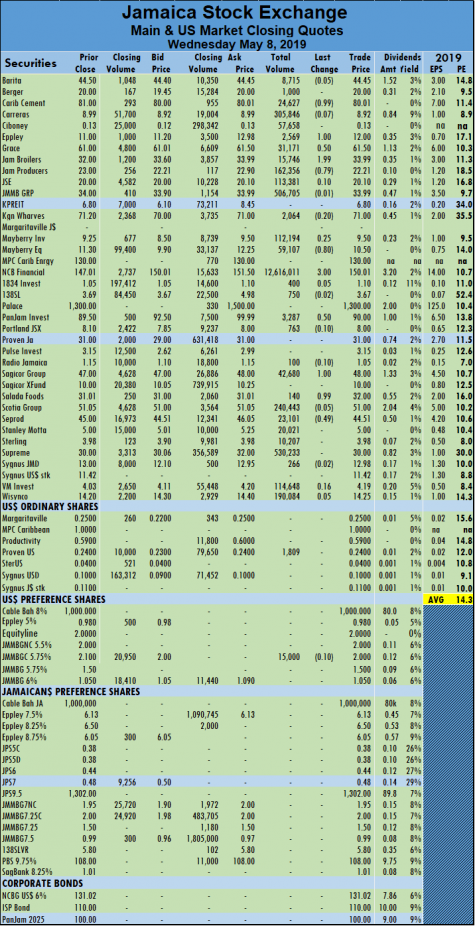

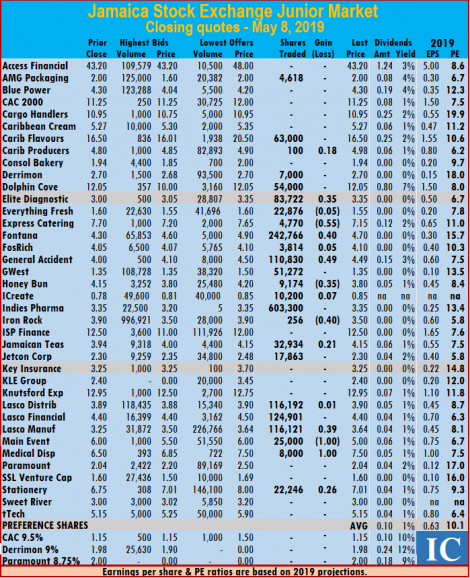

to close at $22.21. JMMB Group added $2 trading 56,642 shares in closing at $34, Mayberry Investments rose 25 cents to end trading of 112,194 shares at $9.50, Mayberry Jamaican Equities shed 80 cents trading 59,107 shares at $10.50, NCB Financial Group climbed $3, in trading 12,616,011 shares, to close at $150.01. PanJam Investment concluded trading of 3,287 shares and gained 50 cents to end at $90, after trading at a record high of $100, Sagicor Group gained $1 to end at $48 trading 42,680 stock units, Salada Foods rose 99 cents to end at $32 after trading 140 shares and Seprod declined 49 cents trading 23,101 shares to close at $44.51.

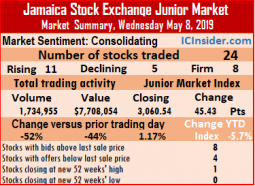

to close at $22.21. JMMB Group added $2 trading 56,642 shares in closing at $34, Mayberry Investments rose 25 cents to end trading of 112,194 shares at $9.50, Mayberry Jamaican Equities shed 80 cents trading 59,107 shares at $10.50, NCB Financial Group climbed $3, in trading 12,616,011 shares, to close at $150.01. PanJam Investment concluded trading of 3,287 shares and gained 50 cents to end at $90, after trading at a record high of $100, Sagicor Group gained $1 to end at $48 trading 42,680 stock units, Salada Foods rose 99 cents to end at $32 after trading 140 shares and Seprod declined 49 cents trading 23,101 shares to close at $44.51. The Junior Market of the Jamaica Stock Exchange made good gains in trading on Wednesday, leading to a strong 45.43 points rise in the market index to close at 3,060.54 but with 52 percent less volume than on Tuesday.

The Junior Market of the Jamaica Stock Exchange made good gains in trading on Wednesday, leading to a strong 45.43 points rise in the market index to close at 3,060.54 but with 52 percent less volume than on Tuesday.  Trading ended with an average of 72,290 units for an average of $321,169 in contrast to 129,846 units for an average of $490,337 on Tuesday. The average volume and value for the month to date amounts to 108,262 units valued at $359,706 and previously, 115,060 units valued at $366,988. In contrast, April closed with an average of 87,963 units valued $317,267 for each security traded.

Trading ended with an average of 72,290 units for an average of $321,169 in contrast to 129,846 units for an average of $490,337 on Tuesday. The average volume and value for the month to date amounts to 108,262 units valued at $359,706 and previously, 115,060 units valued at $366,988. In contrast, April closed with an average of 87,963 units valued $317,267 for each security traded. 9,174 shares and lost 35 cents to end at $3.80, iCreate closed trading of 10,200 shares with a gain of 7 cents to end at 85 cents, Indies Pharma exchanged 603,300 shares at $3.35, Iron Rock settled with a loss of 40 cents at $3.50, with 256 shares. Jamaican Teas closed 21 cents higher at $4.15, with 32,934 units changing hands, Jetcon Corporation finished trading at $2.30, in exchanging 17,863 shares. Lasco Distributors traded 116,192 units for 1 cent higher, at $3.90, Lasco Financial settled at $4.40, trading 124,901 shares, Lasco Manufacturing ended with a rise of 39 cents to $3.64, with the trading of 116,121 shares,

9,174 shares and lost 35 cents to end at $3.80, iCreate closed trading of 10,200 shares with a gain of 7 cents to end at 85 cents, Indies Pharma exchanged 603,300 shares at $3.35, Iron Rock settled with a loss of 40 cents at $3.50, with 256 shares. Jamaican Teas closed 21 cents higher at $4.15, with 32,934 units changing hands, Jetcon Corporation finished trading at $2.30, in exchanging 17,863 shares. Lasco Distributors traded 116,192 units for 1 cent higher, at $3.90, Lasco Financial settled at $4.40, trading 124,901 shares, Lasco Manufacturing ended with a rise of 39 cents to $3.64, with the trading of 116,121 shares,  Jamaica Producers sale of 30 percent of JP Snacks Caribbean, for $720 million add to the group’s cash pile for the Group bringing it to just over $6 billion.

Jamaica Producers sale of 30 percent of JP Snacks Caribbean, for $720 million add to the group’s cash pile for the Group bringing it to just over $6 billion. Tortuga International had revenues of $879 million in 2018, down from $907 million in 2017, according to the group’s audited accounts. Hall attributes the decline to the effects that hurricanes in the region on tourism traffic to some countries within the region.

Tortuga International had revenues of $879 million in 2018, down from $907 million in 2017, according to the group’s audited accounts. Hall attributes the decline to the effects that hurricanes in the region on tourism traffic to some countries within the region.

trading of 1,625 shares at $10.25, Sagicor Financial closed 16 cents lower and completed trading of 124 shares at $8.74 and Scotiabank concluded trading with a loss of 4 cents at $63.51, with 2,500 stock units changing hands.

trading of 1,625 shares at $10.25, Sagicor Financial closed 16 cents lower and completed trading of 124 shares at $8.74 and Scotiabank concluded trading with a loss of 4 cents at $63.51, with 2,500 stock units changing hands. The main market of the Jamaica Stock Exchange moved further ahead in early trading on Wednesday to record new records.

The main market of the Jamaica Stock Exchange moved further ahead in early trading on Wednesday to record new records.

Sagicor Group gained $1.50 to end at $47 trading of 24,788 stock units, Sagicor Real Estate Fund rose $1.50 to end at $10 after trading 11,725 shares. Scotia Group gained 30 cents trading 12,210 shares to close at $51.05. Stanley Motta lost 30 cents in trading 1,172 shares in closing at $5, Supreme Ventures jumped 50 cents and finished at $30, with 812,464 units changing hands, Sygnus Credit Investments climbed $1 with 4,820 units trading, to end at $13 and Wisynco Group lost 30 cents trading 518,941 shares at $14.20.

Sagicor Group gained $1.50 to end at $47 trading of 24,788 stock units, Sagicor Real Estate Fund rose $1.50 to end at $10 after trading 11,725 shares. Scotia Group gained 30 cents trading 12,210 shares to close at $51.05. Stanley Motta lost 30 cents in trading 1,172 shares in closing at $5, Supreme Ventures jumped 50 cents and finished at $30, with 812,464 units changing hands, Sygnus Credit Investments climbed $1 with 4,820 units trading, to end at $13 and Wisynco Group lost 30 cents trading 518,941 shares at $14.20.

In contrast, April closed with an average of 87,963 units valued $317,267 for each security traded.

In contrast, April closed with an average of 87,963 units valued $317,267 for each security traded. with a fall of 8 cents to end at all-time low of 78 cents. Indies Pharma gained 23 cents to close at $3.35, in exchanging 185,468 shares, Jetcon Corporation traded 12,360 shares band declined 20 cents to close at $2.30, Knutsford Express exchanged just 600 shares and lost 5 cents to end at $12.95, Lasco Distributors rose 3 cents to end at $3.89, with 23,874 units changing hands. Lasco Financial closed with a gain of 15 cents at $4.40, with an exchange of 52,032 shares, Lasco Manufacturing added 5 cents trading 30,200 to close at $3.25, Main Event traded 10,000 and closed at $6, Medical Disposables finished trading 19,000 stock units with a loss of 50 cents at $6.50. Paramount Trading closed at $2.04, with exchange of 23,245 units, SSL Venture Capital ended 10 cents higher at $1.60, while trading of 8,500 shares and tTech loss of 3 cents trading 46,823 shares to close at $5.15.

with a fall of 8 cents to end at all-time low of 78 cents. Indies Pharma gained 23 cents to close at $3.35, in exchanging 185,468 shares, Jetcon Corporation traded 12,360 shares band declined 20 cents to close at $2.30, Knutsford Express exchanged just 600 shares and lost 5 cents to end at $12.95, Lasco Distributors rose 3 cents to end at $3.89, with 23,874 units changing hands. Lasco Financial closed with a gain of 15 cents at $4.40, with an exchange of 52,032 shares, Lasco Manufacturing added 5 cents trading 30,200 to close at $3.25, Main Event traded 10,000 and closed at $6, Medical Disposables finished trading 19,000 stock units with a loss of 50 cents at $6.50. Paramount Trading closed at $2.04, with exchange of 23,245 units, SSL Venture Capital ended 10 cents higher at $1.60, while trading of 8,500 shares and tTech loss of 3 cents trading 46,823 shares to close at $5.15.

West Indian Tobacco recovered the $3 lost on Monday to close back at the 52 weeks’ high of $110 on Tuesday, on the Trinidad & Tobago Stock Exchange on a day when rising stocks outnumbered declining ones by a big margin.

West Indian Tobacco recovered the $3 lost on Monday to close back at the 52 weeks’ high of $110 on Tuesday, on the Trinidad & Tobago Stock Exchange on a day when rising stocks outnumbered declining ones by a big margin.  Sagicor Financial finished trading with a rise of 10 cents to end at $8.90, after exchanging 38,894 shares, Trinidad & Tobago NGL closed with a gain of 10 cents and completed trading 3,405 units at $29.50 and West Indian Tobacco advanced $3 and ended at $110, with 260 stock units changing hands.

Sagicor Financial finished trading with a rise of 10 cents to end at $8.90, after exchanging 38,894 shares, Trinidad & Tobago NGL closed with a gain of 10 cents and completed trading 3,405 units at $29.50 and West Indian Tobacco advanced $3 and ended at $110, with 260 stock units changing hands.